Over the next two decades, we’re going to witness something unprecedented: The Great Wealth Transfer.

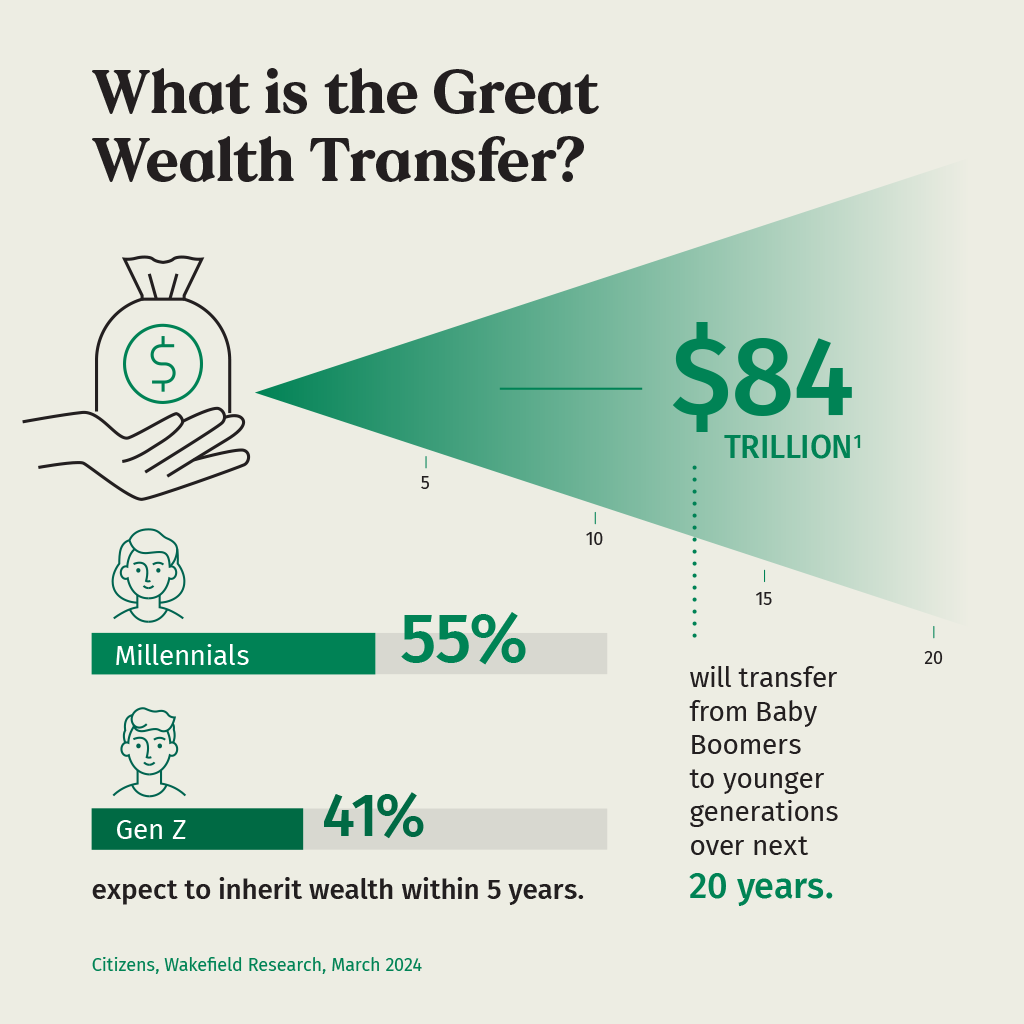

An estimated $84 TRILLION is expected to move from Baby Boomers to their Gen X, Millennial, and Gen Z children and grandchildren over the next 20 years — making it the greatest wealth transfer in history.

For some families, this transfer will be smooth, tax-efficient, and aligned with their values. For others… this may result in confusion, missed opportunities, or unintended consequences — especially if planning has been overlooked or delayed.

If you’re part of the generation preparing to pass down wealth, now is the time to clarify your legacy goals and ensure your financial plan supports them. If you’re expecting to receive or inherit wealth in the coming years, financial education and proactive coordination are key to managing it wisely.

At Towerpoint Wealth, we help clients on both sides of this transfer navigate the financial, emotional, and logistical challenges involved — from structuring and coordinating thoughtful estate plans to avoiding unnecessary taxes and helping families stay aligned across generations.

In this article, we’ll talk about why the great wealth transfer is such a big deal, the most common mistakes families make, and how fiduciary estate and financial planning can help ensure your family’s wealth doesn’t just survive the transition, but grows stronger because of it.

Why is This Transfer So Monumental?

We’re not just talking about a typical shift in wealth from one generation to the next — we’re talking about the greatest wealth transfer in history.

Over the next 20 years, roughly $84 trillion is expected to change hands, primarily from Baby Boomers to their Gen X, Millennial, and Gen Z heirs. And this isn’t just some future event… It’s already happening.

Where is all that wealth coming from?

- Real estate: Homes, vacation properties, and investment properties make up a significant portion of generational wealth.

- Retirement accounts: 401(k)s, IRAs, and pensions that have grown over decades are now being passed on.

- Investment portfolios: Many Boomers have built substantial brokerage and taxable investment accounts that are expected to be inherited by heirs.

- Privately held businesses: A large number of family businesses are in ownership transitions as owners age.

- Life insurance & trusts: Policies and trust assets that are structured to benefit heirs are now activating.

But while this transfer may be MASSIVE in scale, not every family is equally prepared for it.

Some inheritances will arrive with thoughtful planning, coordinated strategies, and clear communication. Others, on the other hand, will be delayed by probate, diminished by taxes, or even lead to disputes between family members due to a lack of clarity and communication.

At Towerpoint Wealth, we often say that the size of your estate isn’t what determines success — it’s the strength of your plan. With the greatest wealth transfer in history already underway, the families who take the time to prepare will be in the best position to preserve and build on what’s being passed down.

Common Mistakes Families Make When Passing Down Wealth

The transfer of intergenerational wealth can be one of the most meaningful — or most stressful — financial events a family experiences. Too often, even well-intentioned families make avoidable mistakes that lead to delays, unnecessary taxes, confusion, or even conflict.

Outdated or Missing Estate Plans

One of the most common issues we see is a lack of current, comprehensive estate planning documents. Families often rely on a will that hasn’t been reviewed in decades — or worse, they assume verbal instructions are enough. Without current legal documents in place, assets can be delayed in probate, decisions may be contested, and your wishes might not be followed the way you intended.

Lack of Communication with Heirs

Just as important is communication.

Even when the legal pieces are in place, communication breakdowns can cause just as much harm. If your heirs aren’t informed about your plan — or don’t understand your intentions — they’re left to guess. This often leads to conflict, confusion, and poor financial decisions. Having open conversations about your legacy goals helps reduce uncertainty and builds trust within the family.

Misaligned Account Titling and Beneficiaries

Another area that causes major disruption? Improper account titling and outdated beneficiary designations. Even with a detailed estate plan, these technical details can override your wishes if they’re not aligned. A retirement account with an ex-spouse still listed as a beneficiary, for example, will go to that individual — regardless of what the will says.

Overlooking Tax Strategies

Taxes play a critical role in wealth transfer. Missing opportunities for a step-up in basis, ignoring capital gains implications, or failing to plan for estate taxes can significantly reduce the amount passed on. Coordinating with a fiduciary financial advisor and a CPA helps to ensure your plan is as tax-efficient as it is well-intentioned.

Focusing on Assets, Not Legacy

At its core, wealth transfer isn’t just about dividing up money. It’s about preserving what you’ve built, reinforcing your values, and empowering the next generation. When families treat it as a transaction instead of a long-term legacy, inheritances are more likely to be misused or misunderstood.

At Towerpoint Wealth, we help clients plan not only for what they want to pass on, but why and how. A well-orchestrated financial plan helps to reduce risk, prevent costly mistakes, and pass down their assets in a way that aligns with their legacy.

Preparing to Pass Down Wealth (For Givers)

If you’re part of the generation preparing to pass down your wealth, the decisions you make today can have ripple effects for decades to come.

Thoughtful planning is about much more than minimizing taxes or avoiding probate. When done right, your planning should ensure your wealth supports the people and causes you care about, in the way you intended.

Here’s where to start:

1. Clarify Your Legacy Goals

Before diving into the logistics, take a step back and define what success really means to you.

Do you want to ensure a smooth, tax-efficient transfer to your heirs? Support charitable causes that matter to you? Help fund your grandchildren’s education? Protect assets from misuse or mismanagement?

There’s no right answer here, but being clear about your priorities will shape every other decision you make. Your financial advisor can help you turn those priorities into a plan.

2. Create or Update Your Estate Plan

If you don’t yet have a full estate plan, or if it’s been years since you’ve reviewed it, now’s the time.

A will alone often isn’t enough. Work with your estate planning attorney and fiduciary financial advisor to ensure your plan includes updated documents, coordinated account titling, and (if applicable) properly funded trusts. An unfunded trust is one of the most common — and costly — estate planning mistakes we see.

3. Plan for Taxes

From estate and gift taxes to capital gains and the step-up in cost basis, tax planning and coordination plays a major role in wealth transfer.

Many families unintentionally trigger tax bills that could have been avoided with proactive planning. A fiduciary financial advisor helps identify those risks and collaborates with your CPA to implement strategies that preserve more of your wealth for your beneficiaries and your legacy.

4. Talk to Your Family

Transparency and communication are two of the most underused — and powerful — tools in coordinated wealth transfer planning.

You don’t have to share every detail, but having open conversations about your goals and intentions can help reduce confusion and avoid conflict later. At Towerpoint Wealth, we often help facilitate these conversations, giving families a safe, objective, and guided environment to talk about money, expectations, and the future.

5. Leverage Gifting and Philanthropy Strategies

Gifting during your lifetime can be a powerful way to support loved ones or causes while reducing the size of your taxable estate. Annual gift tax exclusions, 529 college savings plans, charitable remainder trusts, and donor-advised funds are just a few of the tools available.

But the real value isn’t just in the tax benefits — it’s in the opportunity to see your impact while you’re here, and to lead by example.

Passing down wealth is a personal event just as much as it is a financial one. And with the right guidance, it can be one of the most meaningful parts of your financial journey.