Over the past few weeks, many families have started asking about a new Trump investing account being discussed in connection with the recently passed One Big Beautiful Bill Act (OBBBA).

Questions are coming from all directions: parents, grandparents, and even adult children trying to understand what this type of child savings account actually is, and whether it should factor into longer-term financial and investment planning.

The reaction is understandable. Anytime the government introduces a new savings vehicle for children — particularly one positioned as an infant savings and investing plan — it naturally raises broader questions.

Who controls the account? How flexible is it over time? And how does it fit alongside the strategies families may already be using?

This conversation isn’t about politics, and it isn’t about whether any single account is “good” or “bad.” It’s about context. New savings tools can be useful, but only when they’re evaluated within the bigger picture of planning, control, and longer-term intent.

In this article, we’ll walk through what these accounts are designed to do, how they differ from other child saving and investing options, and what families may want to consider when thinking about generational planning — without assumptions, urgency, or speculation.

What Are Trump Accounts?

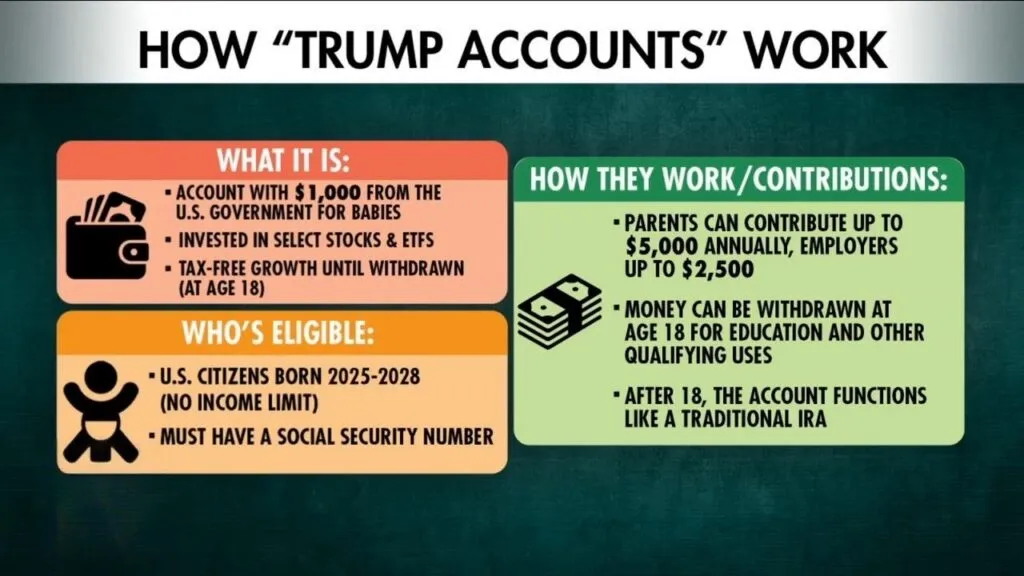

At a high level, Trump Accounts — sometimes referred to as Trump child savings accounts — are a newly proposed federal savings vehicle designed for children.

The concept is relatively straightforward: an account established early in a child’s life, seeded with an initial government contribution (if the child is born between 1.1.2025 and 12.31.2028), with the option for families and others to add funds over time.

The intent behind these accounts is longer-term investment growth and compounding. They’re not designed for shorter-term spending or near-term economic needs, but rather to support future milestones later in life for the child. In that sense, they can fit into the broader category of infant and children’s savings plans that aim to give children an early financial starting point.

What’s important to understand at this stage is that this structure is still developing. Many of the features being discussed are tentative, and their real-world impact will depend on how the program is ultimately implemented.

Based on current guidance, Trump savings accounts are expected to include:

- A one-time government contribution at birth for eligible children.

- Annual contribution limits, currently discussed at up to $5,000 per year.

- The ability for parents, grandparents, or others to contribute within those limits.

These caps may be a meaningful feature for some families — and a constraint for others — depending on how the account is used alongside existing planning tools.

How to Set Up a Trump Account

Opening a Trump account is expected to involve a dedicated filing process. Current guidance points to Form 4547, filed alongside a federal tax return, as the primary mechanism for establishing the account.

As with many new programs, the ease of the Trump account setup, ongoing administration, and custodial options will play a significant role in how practical these accounts become over time.

IRA Conversion and Long-Term Flexibility

Another tentative feature that’s receiving attention is the ability to convert Trump account assets to an IRA once the beneficiary reaches adulthood, subject to future rules and limitations.

If implemented as proposed, this could introduce longer-term flexibility — but the details around timing, eligibility, and coordination with other retirement accounts remain important unknowns.

Employer Matches and Private Contributions

Some proposals also reference employer matching contributions or private donations, including highly publicized commitments from prominent individuals.

While these elements are drawing attention, they are not guaranteed features for every account and may vary significantly based on employer participation, policy interpretation, or future rulemaking.

Why the Details Matter

Taken together, these features explain why Trump savings accounts are best viewed as a framework, not a complete strategy.

Contribution limits, filing mechanics, conversion rules, and third-party incentives all shape how useful an account may be — and for whom. As with any new planning tool, the structure matters just as much as the headline.

Understanding what the account is designed to do is the first step. Deciding how it may or may not fit into a family’s broader planning picture is a separate conversation — one that benefits from context, patience, and a longer-term perspective.

How Trump Child Savings Accounts Differ From Other Children’s Savings Plans

Anytime a new child savings account enters the conversation, the natural question follows: How is this different from what already exists?

It’s important to keep in mind that Trump child savings accounts aren’t replacing other children’s savings plans — they’re adding another option to an already existing landscape.

Other Child Savings Options

529 plans, for example, are education-focused by design. They work well when the primary goal is funding qualified education expenses, but their usefulness is tied closely to how and where funds are ultimately used.

Custodial accounts, like UGMA or UTMA accounts, are more flexible in how funds can be used, but they also come with a clear tradeoff: control shifts to the child at a legally defined age. For families thinking longer-term, that timing element is often just as important as the tax or investment features.

Trust-based planning exists on the opposite end of the spectrum. Trusts allow for highly customized control, distribution rules, and longer-term intent — but they also introduce more complexity, administration, and cost.

They’re often used to solve for governance and legacy, not simplicity.

What Sets Trump Accounts Apart?

Trump savings accounts appear to sit somewhere in between. They’re designed for longer-term growth rather than a single predefined use, while still operating within a standardized federal framework.

The government-seeded starting point is a notable distinction, but the longer-term impact will depend on how contribution rules, access, and oversight are ultimately defined.

From a planning perspective, the takeaway is straightforward: each savings plan solves a different problem. Education funding, early financial exposure, control over timing, and longer-term wealth transfer are not the same objective — even though they’re often grouped together.

That’s why no single child savings account replaces thoughtful family financial planning. These tools are most effective when they’re understood in context, not evaluated in isolation.

Why These Accounts Are Getting Attention in Family Financial Planning

The interest around Trump savings accounts isn’t really about the account itself — it’s about what it represents. As we get further into 2026, more families are thinking beyond education funding and asking broader questions about how, when, and why wealth is introduced to the next generation.

As early savings vehicles gain visibility, they naturally surface planning considerations that extend well past childhood. Questions around control, timing, and responsibility tend to come up quickly:

- Who manages the account?

- When does access change?

- How does early financial support shape long-term behavior and expectations?

From a family financial planning perspective, these conversations often trigger a shift. Families aren’t just asking how to save — they’re clearly thinking about intent. They’re thinking:

- What role should early assets play in adulthood?

- How much structure is appropriate?

- How does this fit into a broader picture of longer-term wealth and decision-making?

In that sense, Trump savings accounts function as a conversation starter, not a standalone solution. They invite families to step back and think more intentionally about generational planning — how different tools work together, and how early decisions can influence outcomes years down the road.

Trump Savings Accounts and Generational Wealth Transfer

When families think about generational wealth transfer, the conversation often centers on timing, when assets are passed, and in what form.

Early savings vehicles like Trump savings accounts add another layer: how early exposure to wealth fits into a longer-term plan.

Starting early can be a powerful lever. Time, compounding, and consistency all work in your favor. But early funding alone doesn’t define the outcome. What ultimately matters is how that account is coordinated with the rest of the family’s financial picture.

There’s an important distinction here. Giving assets is not the same as creating structure that can be passed on. One focuses on the transfer itself. The other considers how responsibility, decision-making, and longer-term intent are shaped along the way.

Without context, even well-funded accounts can feel disconnected from broader family goals.

From a planning perspective, early savings vehicles are most effective when they’re viewed as one piece of a larger system. How they interact with education planning, estate structures, gifting strategies, and future support decisions matters just as much as the account balance itself.

That’s why we believe that intentionality outweighs the specific account type. When early savings and investing are aligned with a family’s longer-term vision — rather than added in isolation — they can support generational wealth transfer in a way that feels thoughtful, measured, and consistent over time.

Considerations Families Should Think Through

Any time a new program enters the conversation — especially one that includes a government contribution — it’s tempting to view it as free cash. But with a Trump savings account, thoughtful family financial planning still matters.

Longevity and Policy Stability

Any new savings vehicle tied to legislation comes with an open question of: how stable will the rules be over time?

Contribution limits, access rules, tax treatment, and administrative details may evolve as policies change. Families considering a Trump savings account should view it as a longer-term structure that may adapt, rather than a fixed set of rules that will look the same decades from now.

How It Interacts With Existing Planning

Most families already have planning tools in place — 529 plans, custodial accounts, trusts, or gifting strategies. A Trump child savings account shouldn’t exist in isolation.

Its role depends on how it complements (or complicates) those existing structures, particularly when multiple accounts are intended to support the same longer-term goals.

Control, Timing, and Access

Early savings vehicles naturally raise questions about who controls the assets, when access begins, and how responsibility is introduced.

These aren’t technical details to ignore, but critical aspects that can shape outcomes. The structure of access can influence how funds are ultimately used and how expectations are formed, long before the child reaches adulthood.

Behavioral and Family Dynamics

Money introduced early — especially when framed as “foundational” or “guaranteed” — can shape behavior, even if subtly. Families often want savings to encourage opportunity and responsibility, not entitlement. How an account is positioned within the family narrative can matter just as much as how it’s funded.

Fit Within a Broader Family Financial Plan

A Trump savings account may be helpful in the right context, but, as with any new tool, it’s rarely the full answer. Its effectiveness depends on how well it aligns with cash flow priorities, tax planning, estate considerations, and longer-term family intentions.

When those pieces are coordinated, new tools can enhance a plan rather than distract from it.

Final Thoughts

New ideas and new accounts tend to generate a lot of attention, especially when they’re positioned as early opportunities.

At Towerpoint, we don’t view tools like a Trump child savings account as replacements for thoughtful planning. We evaluate them in context — alongside cash flow, tax coordination, estate considerations, and longer-term flexibility — to understand whether they genuinely support a family’s broader goals.

As tempting as it may be, longer-term financial planning isn’t about chasing every new option as it appears. It’s all about having a framework that can absorb new tools without giving them the steering wheel.

When that framework is in place, accounts like this can be assessed calmly and objectively in the context of a greater financial plan, rather than reactively.

From a generational wealth transfer perspective, early savings vehicles can become meaningful over time — but only when they’re integrated intentionally. The structure of the account, how it interacts with other planning decisions, and the expectations it creates all matter. Starting early can be powerful, but outcomes depend on coordination, not timing alone.

If you’re curious about how a Trump savings account fits into your existing strategy, a conversation can help put it in perspective. Understanding the structure early often leads to more grounded, better-aligned decisions down the road.

We invite you to schedule a complimentary 20-minute “Ask Anything” conversation with our team, where we can see how we can support your financial planning for your family.