As a small business owner, we know that you are an “around the clock” grinder, with a myriad of responsibilities that often supersede the core responsibilities you have to the growth of your business. And understanding that a regular review of your business’s retirement plan may not be a top priority of yours, at Towerpoint Wealth we have created this 401(k) “healthcheck” for your benefit. We regularly come across 401(k) and other company-sponsored retirement plans that, as currently structured, are in serious need of attention and improvement, and we are experienced in helping you, as a trustee and fiduciary to your company’s retirement plan, minimize the hassle of giving your plan the attention it needs.

Is your 401(k) plan structured and optimized properly to help you and your employees maximize the myriad of economic, investment, and tax benefits? Are you properly managing your fiduciary responsibility? Ask yourself the questions found below to quickly gauge whether your 401(k) needs adjusting or improving.

Does my plan have a safe harbor structure?

You want to ensure that your 401K) retirement plan passes the annual non-discrimination testing conducted by the IRS. In its simplest sense, non-discrimination testing ensures that an employer is making contributions to each employee’s retirement account that equals the same percentage of salary for everyone. Importantly, if a plan fails a non-discrimination test, the 401(k) may lose its tax-qualified status.1

[1]The most common reason a 401(k) plan fails this non-discrimination testing is when one or more of the business owners make much greater 401(k) contributions compared to their employees.

A safe harbor 401(k) plan structure ensures that you meet the non-discrimination regulatory requirements by following strict guidelines specific-to employer plan contributions, participant disclosures, and much more.

Does my plan have a profit-sharing component and if so, am I optimizing its structure?

For a business owner to maximize the personal net worth building benefits associated with sponsoring a company retirement plan and receive the maximum 401(k) annual contribution amount of $58,000 in 2021[1] (employee deferrals + employer contributions), pairing a profitsharing component in the plan’s design is essential.

All profit sharing plan structures – same dollar amount, comp-to-comp, new comparability, etc.[2] – are not created equal. In particular, the new comparability strategy is becoming increasingly more common in modern 401(k) plans as this type of profit-sharing plan allows for unique flexibility in allocating the profits among the business owner(s) and employees.

Is my investment fund lineup optimized?

401(k) investment fund lineups vary from basic to advanced and passive to active. And with employees having better and more diverse investment options outside of 401(k) plans, annually reviewing your company’s fund lineup for improvements is critical to ensure that employees do not look to invest their hard-earned dollars elsewhere, and also to meet your fiduciary responsibility as plan trustee.

It is also a requirement that a business owner (usually with help from an investment professional) formulate, and review at least annually, an investment policy statement (IPS) for their 401(k).

Is my ERISA fidelity bond fund amount appropriate?

The Employee Retirement Income Security Act (ERISA) requires 401(k) plans to hold a fidelity bond, which protects the plan from losses resulting from improper handling of the funds.

While fidelity bonds are generally inexpensive for the coverage offered, we often see the amount protected as either 1.) inadequate or 2.) overkill.

[1] Increased to $64,500 for business owners 50 years of age or older.

[2] There are often several different terms that refer to the exact same type of profit-sharing structure.

Does my plan currently allow for after-tax Roth contributions?

While changing for the better, many 401(k) plans still do not allow after-tax Roth contributions.

For business owners and employees that are in a temporarily low income tax bracket – a business owner “winding down” and closing in on retirement or a younger employee at the beginning of their career and earning curve – offering an after-tax Roth contribution option, particularly given it typically costs nothing to do so, is a valuable and often overlooked plan benefit.

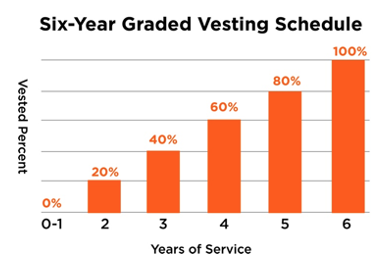

Is my vesting schedule appropriate?

In order to incentivize employees to stay with your company, having a vesting schedule for any employer-matching profit sharing contributions that is not overly generous is important. For a number of Towerpoint Wealth’s clients who are business owners, a vesting schedule of six years (with 0% vesting in the first year of participation) is appropriate, but each business and retirement plan is unique.

Have I considered automatically distributing an employee’s 401(k) balance when they leave the company?

Many 401(k) plan administrators charge their fees based on the number of employees that the plan has.

In order to keep fees to a minimum, it is advisable to consider automatically distributing account balances below a certain threshold when an employee separates from service.

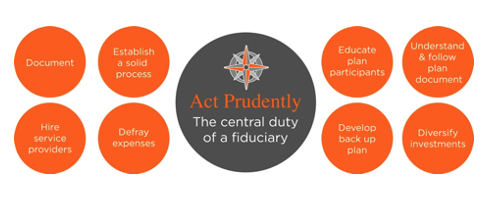

Am I managing my fiduciary responsibility and minimizing my fiduciary liability?

All business owners who offer a 401(k) for themselves and their employees have a fiduciary responsibility to ensure that they are acting in the employees’ best interests, being prudent, diversifying plan investment assets, and adhering to all provisions of the retirement plan documents.

There are concrete steps that a business owner can take to uphold their fiduciary duty and at the same time, minimize their fiduciary liability.

Wealth management firms that specialize in helping business owners optimize their retirement plans, such as Towerpoint Wealth, are able to help guide you through these murky waters.

Am I doing everything I can to maximize my own personal net worth within my company’s retirement plan?

Even if a small business owner has a well-structured plan that meets everyone’s needs, is it important to remember that 401(k)s, and other types of company-sponsored retirement plans, are uniquely customizable. And often, there are overlooked plan features that may help the business owner maximize their ability to accumulate wealth within the plan.

One of these particularly powerful features is allowing for after-tax deferrals (not the same as after-tax Roth deferrals), which then affords the business owner to take advantage of the “Mega Backdoor” Roth IRA strategy.

Some other questions that are worth your thoughtful attention: Do I allow for hardship distributions and if not, should I? What about allowing rollovers from other retirement plans? Is it risky to offer loans to employees? Are my plan’s expenses and fees reasonable?

How Can We Help?

Director of Tax and Financial Planning

At Towerpoint Wealth, we are a legal fiduciary to you, and specialize in optimizing retirement plan structures for business owners.. If you would like to speak with us regarding any other tax questions you may have, we encourage you to call (916-405-9166) or email (spitchford@towerpointwealth.com) to open an objective dialogue.

Towerpoint Wealth, LLC is a Registered Investment Adviser. This material is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Towerpoint Wealth, LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Towerpoint Wealth, LLC unless a client service agreement is in place.