When it comes to investing, many people focus on maximizing returns — finding the right investments, properly diversifying their portfolios, and shrugging off shorter-term market noise. But there’s one factor that can quietly eat away at those gains if not managed properly: TAXES.

Many investment decisions carry tax consequences. Whether it’s capital gains from selling investment positions, dividend payouts, interest income, or capital gain distributions from mutual funds, taxes can significantly impact your after-tax returns. And for high earners, the tax burden can be even greater.

This is where being conscious about tax-efficient investing comes in. A well-structured investment strategy isn’t just about growing your wealth — it’s about keeping more of what you earn.

In this article, we’ll break down the tax implications of investing, explore tax-efficient investing strategies, and discuss how investors — especially higher-net-worth individuals — can minimize that “tax drag” and better protect their portfolios.

Key Takeaways

- Not all investment income is taxed the same way. Understanding how capital gains, dividends, and interest are taxed can help you optimize your after-tax returns.

- Asset location matters. Placing tax-inefficient investments in tax-advantaged accounts, like IRAs and 401(k)s, can significantly reduce your tax burden.

- Tax-efficient strategies can boost longer-term growth. Techniques like tax-loss harvesting, Roth conversions, and the Backdoor Roth IRAs can help minimize taxes and maximize wealth.

- Choosing the right investments for your portfolio is crucial. Tax-efficient mutual funds and ETFs with low turnover can help reduce capital gains taxes.

- Working with your financial and tax advisors can enhance tax efficiency. A strategic, tax-sensitive investment plan ensures you keep more of what you earn.

Why Tax Efficiency Matters for Investors

Tax efficiency is oftentimes overlooked in investment planning, yet it plays a crucial role in longer-term wealth accumulation. While market performance and asset allocation are key factors in portfolio success, taxes can significantly impact your overall net returns.

Not only do you pay taxes on investments, but the way you invest — whether through taxable accounts, tax-advantaged accounts, or specific asset types — can dramatically affect how much you owe and how much of your returns you actually keep.

Without a tax-efficient strategy, investors may find themselves paying more to the IRS than necessary, ultimately reducing their net investment gains. By strategically managing taxes, investors can retain more of their wealth and enhance portfolio growth over time.

Here’s why tax efficiency is critical for investors looking to protect their wealth.

The Erosion of Returns Due to Taxes

Investment gains are not just about how much your portfolio grows but how much you actually keep after taxes.

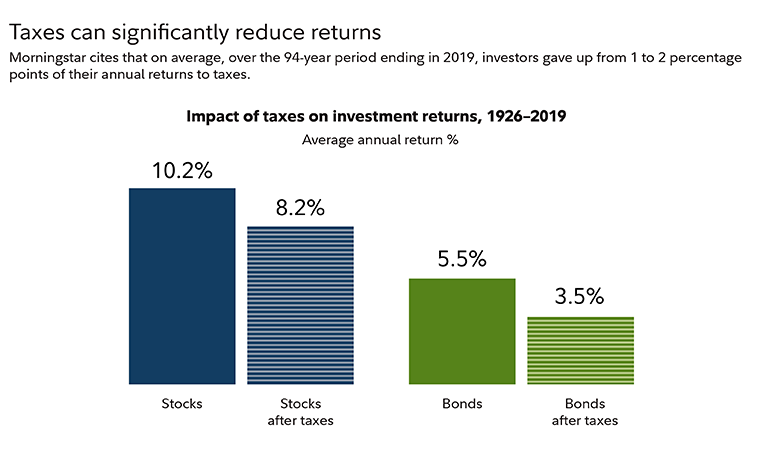

If you earn a 7% return but lose a significant portion of it to taxes, your real return may be much lower than anticipated. Taxes on capital gains, dividends, and interest income can take a sizable chunk out of investment earnings — especially for high-income individuals who may be subject to higher tax rates.

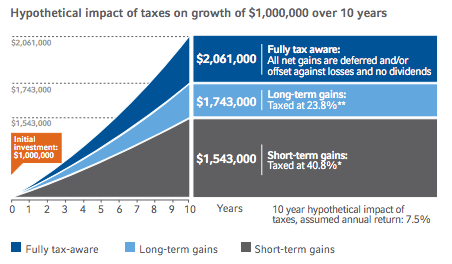

Consider two investors with identical portfolios, one employing tax-efficient strategies and the other ignoring tax implications. Over time, the tax-conscious investor retains more of their earnings, leading to greater compounding and a higher final portfolio value.

What does this mean? The more tax-efficient your investments, the more money you may end up keeping.

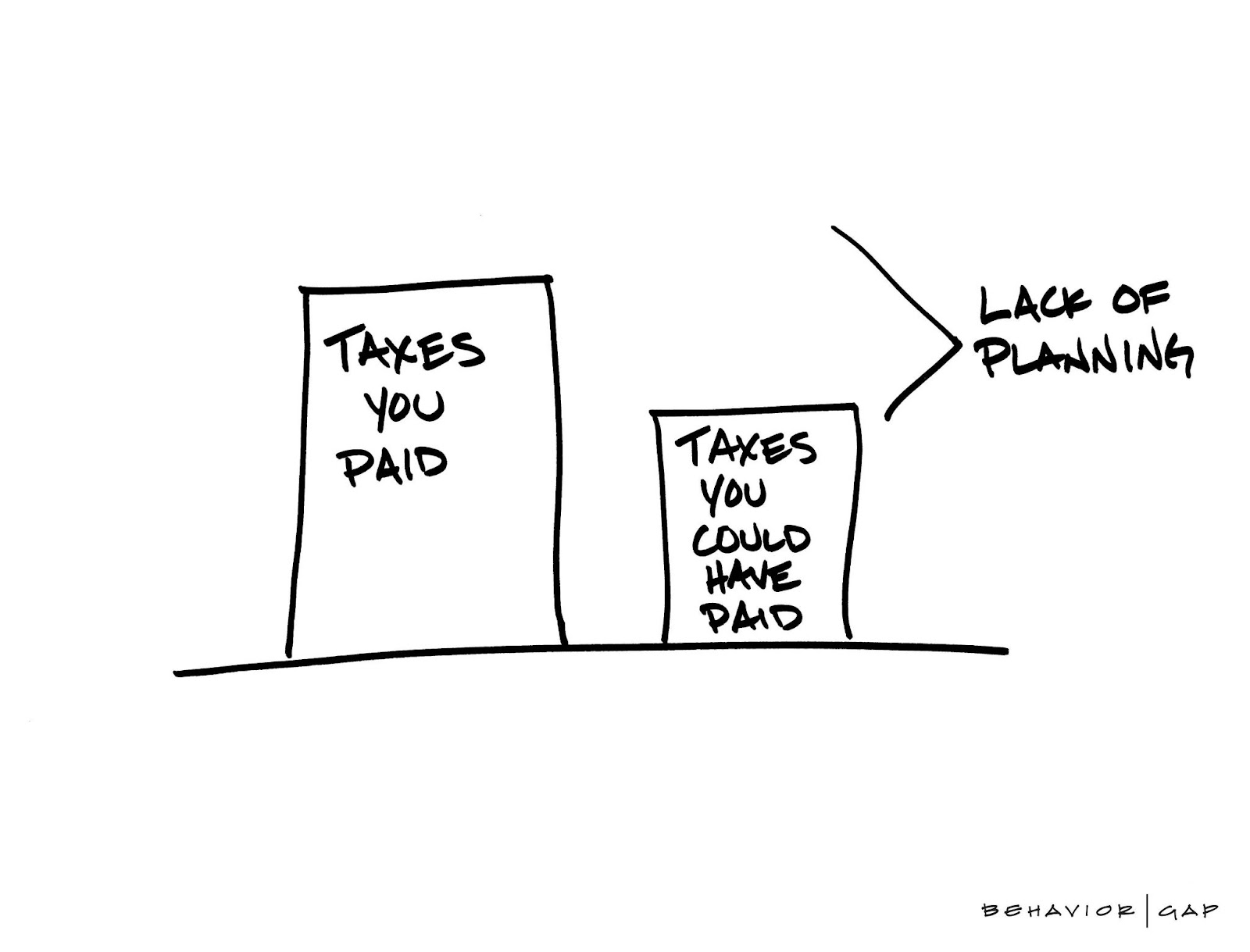

The Impact of Tax Drag on Investment Growth

“Tax drag” refers to the reduction in an investment’s growth due to taxes on interest, dividends, and capital gains.

Mutual funds, for example, often distribute taxable capital gains, forcing investors to pay taxes even if they haven’t sold any shares. This tax drag can slow portfolio growth significantly, particularly in taxable accounts.

By investing in tax-efficient vehicles such as ETFs, which generate fewer capital gains distributions, or holding higher-growth assets in tax-advantaged accounts, investors can reduce tax drag and keep more of their money working for them.

How Different Investments Are Taxed

A common question investors ask is: “Do you pay taxes on investments?”

The short answer? Yes — but how much you pay depends on what you invest in, where you hold your investments, and how you structure your portfolio.

Before diving into strategies, it’s important to understand how taxes on investment income work. Here’s a quick breakdown of what that can look like:

- Capital Gains Taxes

- Short-term capital gains (assets held less than one year) are taxed as ordinary income (up to 37% for high earners).

- Long-term capital gains (assets held more than one year) are taxed at lower rates (0%, 15%, or 20% depending on your income).

- Dividend Taxes

- Qualified dividends are taxed at lower long-term capital gains rates.

- Nonqualified dividends are taxed at higher ordinary income levels.

- Interest Income Taxes

- Interest from corporate bonds, bank savings accounts, REITs, and CDs is taxed at ordinary income rates.

- Interest from municipal bonds is federally tax-free and usually state tax-free, making them a potentially great option for high earners.

- Taxes on Mutual Funds

- Many mutual funds generate capital gains distributions, which investors must pay taxes on — even if they didn’t sell any shares.

Different types of investments have different tax treatments, so it’s important to have strategies in place that help make the most out of every dollar you contribute to your nest egg.