Across tech, banking, and private equity-backed firms, executive transitions are happening more frequently, and often with little warning.

Whether it’s a restructuring, leadership change, or a move to a new opportunity, one thing tends to stay the same:

A wave of financial decisions shows up all at once.

And for high-income professionals, those decisions aren’t isolated.

They affect:

- How income is received

- How equity is handled

- How taxes are triggered

- How benefits need to be replaced or restructured

What makes this challenging isn’t any one decision, but how quickly they all begin to interact.

This is where proactive executive transition planning becomes important. Because once income shifts and timelines change, decisions that might otherwise be spaced out over time often need to be evaluated together.

And without a clear way to think through how those pieces connect, it’s easy for decisions to be made one at a time, often under time pressure, and without a full view of the longer-term impact.

The problem is that this isn’t a single decision to make. It’s a series of deeply interconnected ones.

Why Executive Transitions Create Complex Financial Decisions

An executive transition doesn’t just introduce new decisions; it also changes the structure within which those decisions are made.

During a typical year, income is consistent, equity follows a defined schedule, and benefits operate in the background. Decisions can be made with some separation between them.

That is usually not the case during a transition.

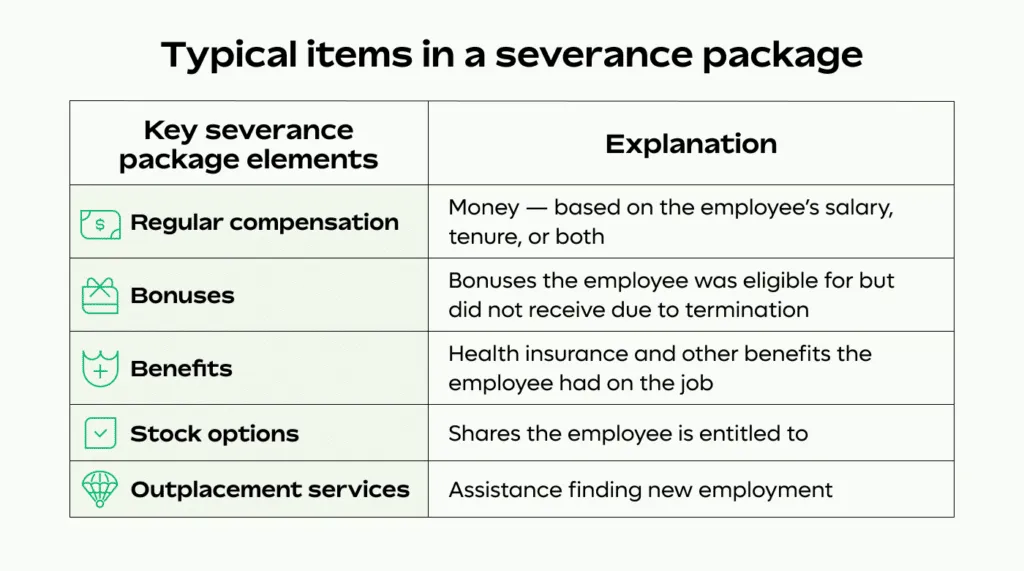

Salary may be replaced by severance, equity timelines can accelerate or be cut short, benefits that were once automatic need to be re-evaluated, and the way income is received — and taxed — can vary more than it has in the past.

Each of these decisions can be worked through on its own, but in practice, they rarely exist in isolation:

- How severance is structured can affect your overall tax exposure.

- Equity decisions can influence liquidity.

- Changes in income can create planning opportunities or constraints, depending on how they’re handled.

This is where complexity tends to show up, because the decisions begin to interact. What might seem like a straightforward choice in one area can have implications across several others.

That’s where most decisions start to get made quickly, and often without the full context of how they connect.

Where Decisions Tend to Get Made Too Quickly

One of the biggest challenges with an executive transition is timing.

Many of the decisions that come up aren’t open-ended — they come with deadlines, constraints, or a limited window to act. Severance agreements often need to be signed within a set period, stock options may have a defined post-termination exercise window, and benefits decisions (like COBRA) are presented as immediate next steps.

Individually, these decisions are manageable. But it becomes much more complex when they all happen at the same time.

It’s not uncommon for someone to review a severance package and focus on the headline numbers without fully considering how the structure affects taxes. Or to make a decision around stock options based on timing alone, without factoring in liquidity or broader planning implications. Benefits decisions are often handled quickly, as well, simply to ensure coverage continues without interruption.

The challenge is that these choices are often made under time pressure, without a clear framework for how they connect. That’s where things can start to feel fragmented.

Decisions get made as they come up, each one addressed on its own timeline. And while each step may make sense in the moment, the overall result isn’t always as coordinated as it could be once everything is put together.

The Decisions That Carry the Most Weight

Once everything is on the table, a handful of decisions tend to drive the majority of the outcome.

They don’t always stand out at first. But these are the areas where timing, structure, and coordination can have a meaningful impact — especially when they’re evaluated in the context of everything else happening at the same time.

How Is Severance Pay Taxed for Executives?

Severance is often the first major decision — and one that’s often misunderstood from a tax perspective — and it’s easy to focus on the total value rather than how it’s paid.

A lump sum may push more income into a single tax year, potentially increasing marginal rates. Spreading payments over time can change that outcome, but may introduce trade-offs depending on how future income is expected to look.

What matters here isn’t just the amount — it’s how the structure fits alongside other income, and how that timing carries through the rest of the plan.

What Happens to RSUs When You Leave a Company?

Restricted Stock Units (RSUs) tend to follow a defined vesting schedule, but that schedule typically changes once employment ends.

Unvested shares may be forfeited, while vested shares are typically taxed as income. The timing of that income — and how it overlaps with other compensation — can influence the broader tax picture more than it appears at the surface.

This is one of the areas where decisions may feel straightforward, but still benefit most from being viewed in the context of your overall transition planning.

What Should I Do With Stock Options After Termination?

Stock options introduce a different kind of timing pressure in periods of transition.

Post-termination exercise windows can be limited, particularly for Incentive Stock Options (ISOs), and deciding whether — or when — to exercise involves more than just market outlook. Tax treatment, liquidity, and concentration risk all come into play.

Once that window closes, the opportunity is gone. So rushed decisions often need to be made with incomplete information, which makes the surrounding context even more important.

What Happens to Deferred Compensation After Leaving a Job?

Deferred compensation plans are usually set up years in advance, but their impact becomes more immediate during a transition.

Distribution timing, tax treatment, and the financial stability of the employer all factor into how those assets are evaluated. In some cases, decisions are locked in. In others, there may be limited flexibility.

Either way, this is an area where understanding how those distributions fit into overall income can make a meaningful difference.

What Are the Best Health Insurance Options After Job Loss?

Health coverage decisions tend to feel administrative, but they can carry real financial implications, especially at higher income levels.

COBRA offers continuity, but often at a higher cost. Private options may provide more flexibility, but require more active comparison. And for many high-income professionals, subsidies aren’t part of the equation.

It’s a decision that often gets made quickly, but still should be weighed alongside the broader financial picture.

Should I Do a Roth Conversion After a Job Transition?

A transition can create a temporary shift in income, which may open the door to planning opportunities that don’t exist in a typical year.

Lower income can make Roth conversions more efficient. In certain cases, strategies like net unrealized appreciation (NUA) may also come into play.

These opportunities aren’t always obvious in the moment, but they tend to have longer-term implications when they’re considered as part of a broader plan.

How Should I Handle Liquidity and Runway Planning?

Underlying all of these decisions is a more practical question: how much flexibility is available in the near term?

Severance, cash reserves, and expected timing of the next role all factor into how much room there is to make decisions deliberately rather than reactively.

When liquidity is clearly pre-defined, it becomes easier to evaluate trade-offs, manage timing, and avoid decisions that are driven by immediate pressure rather than longer-term impact.

How These Decisions Interact

Looking at each decision on its own can make the process feel independent. In reality, they rarely stay contained that way.

A severance package doesn’t just replace income — it changes how that income is taxed in the current year, which can influence whether certain strategies make sense or not. A decision around stock options isn’t just about timing — it can affect how much liquidity is available, which then shapes how flexible other decisions can be.

Even something that feels more tactical, like when income shows up, can carry through into multiple areas of the plan. A higher income year may limit certain opportunities, while a lower one may create them. But those outcomes depend on how the surrounding decisions are structured.

What’s decided in one area tends to narrow, or expand, the range of options in another. That’s why these moments don’t lend themselves well to a checklist approach.

The decisions aren’t independent. They form a system where timing, sequencing, and coordination start to matter just as much as the decisions themselves.

Bringing Structure to the Transition

What makes executive transitions challenging isn’t just the number of decisions, but how closely they’re tied together.

A choice around severance can influence tax exposure in the same year. An equity decision can affect liquidity, which then shapes how much flexibility exists around other timing decisions. What happens in one area doesn’t stay contained for long.

That’s why working through these moments one decision at a time often leads to results that feel fragmented once everything is put together. A more structured approach starts by stepping back and looking at the full picture at once:

- What income is expected this year, and how is it structured?

- Which decisions have fixed deadlines, and which have flexibility?

- How do equity, taxes, and liquidity interact over the next several years, not just the current one?

When those pieces are evaluated together, the trade-offs become clearer. Timing decisions can be made more deliberately. Opportunities that might otherwise be missed — particularly around taxes or income structure — are easier to identify while there’s still time to act.

At Towerpoint Wealth, this is typically how proactive transition planning is approached: by coordinating income, equity, tax, and liquidity decisions within the same framework — and often alongside a CPA when tax considerations are involved.

For many executives, the real value shows up not in any single decision, but in having a clear way to evaluate how those decisions fit together, and how they’re likely to carry through over time.

Final Thoughts

Executive transitions are typically temporary. The decisions that come with them are not.

Income may look different for a period of time, roles may change, and timelines may be uncertain. But the way decisions are handled during that window can carry forward into future tax years, future liquidity, and future flexibility.

That’s what makes these moments worth approaching more intentionally.

When there’s a clear way to evaluate how income, equity, taxes, and timing fit together, it becomes easier to move forward with consistency, even as things change.

If you’re navigating a transition or expect to in the near future, it can be worth stepping back to look at how those decisions are connected, and whether they’re being approached with a clear framework in place.If you’d like to step back and review how these decisions are structured — and how they may carry through over time — we’d be happy to have that conversation. We invite you to schedule a complimentary 20-minute “Ask Anything” conversation with our team, where we can see how coordinated planning can give you confidence and flexibility before, during, and after transitions.