Conversations around Roth IRA conversions tend to come up frequently around retirement planning. They’re often framed in overly simple terms — pay taxes now, avoid them later — and positioned as a way to create more tax-efficient income over time.

You’ll often hear the conversation centered around two core ideas:

- Move money into tax-free accounts while Federal income tax rates are relatively low.

- Create flexibility later by reducing future tax exposure.

And those points are valid at a high level, but they don’t fully answer the question most people are actually trying to solve.

A traditional IRA to Roth IRA conversion has an immediate effect. The amount converted is included in your taxable income in the year it occurs, which can influence tax brackets, planning decisions, and how income is managed across that time period.

The impact of the strategy carries forward from there. The conversion affects how future withdrawals are structured, how different income sources interact, and how other decisions are evaluated alongside it. The same conversion can lead to different outcomes depending on timing, income levels, and how those surrounding decisions are handled.

For that reason, Roth conversions, while a potentially powerful lever, are best evaluated within the full context of a financial plan alongside income, taxes, and withdrawal strategy, rather than as a standalone move.

What a Traditional IRA to Roth IRA Conversion Actually Does

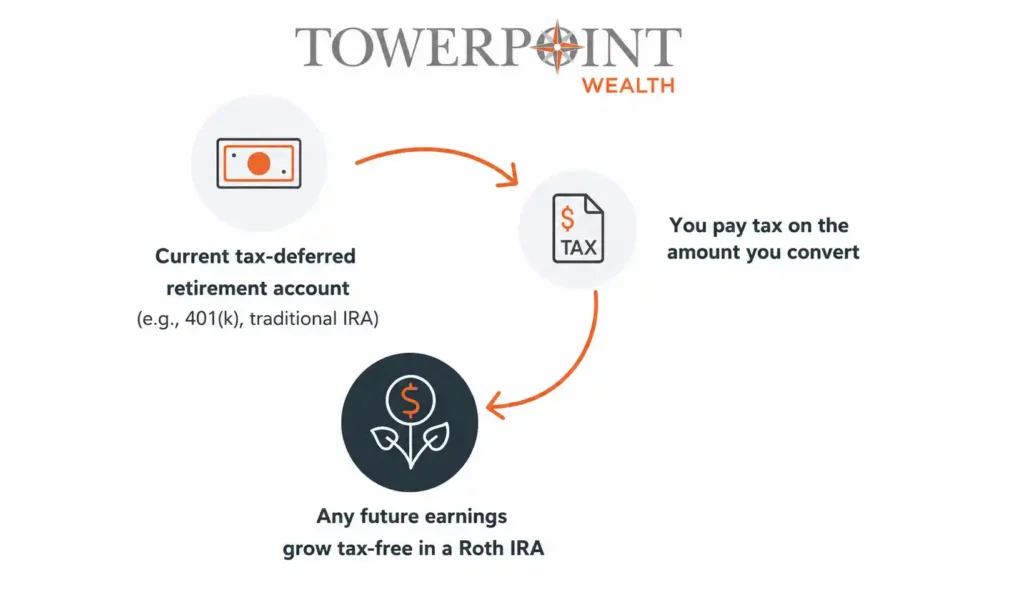

A traditional IRA to Roth IRA conversion changes how retirement assets are taxed down the line.

Inside a Roth conversion, funds that were originally contributed on a pre-tax basis are moved into a Roth IRA, where qualified withdrawals are not subject to income tax. However, at the time of the conversion, the amount transferred is included in taxable income for that year.

So, when you convert a traditional IRA to a Roth IRA, you’re recognizing income today with the understanding that those assets will be treated differently going forward.

The same concept can apply to employer-sponsored plans. A 401(k) to Roth IRA conversion typically involves rolling funds into an IRA and then converting them, with the amount converted taxed in the year the transaction occurs.

From a mechanical standpoint, the process is relatively straightforward, but the real impact depends on how that additional income fits into your broader personal and economic picture.

A conversion doesn’t eliminate taxes from your plate; it simply changes when they’re paid. Bringing that income into the current year can affect tax brackets, other planning decisions, and how income is managed over that period.

The impact of timing is what makes the decision more involved than it may appear. Rather than focusing on whether to convert in isolation, the decision is best centered on how the conversion affects your overall financial plan over time.

What Determines the Impact of a Roth Conversion

While the mechanics of a Roth conversion are consistent, the outcome is not. Several factors influence how a Roth IRA conversion plays out over time, and those factors don’t exist independently of one another.

In practice, the effect of a conversion is shaped by a combination of:

- Tax rates in the year of conversion: The amount converted is added to your taxable income, so where that income falls within your current tax structure can affect your liability.

- How income changes over time: A year with lower income can create more room for a conversion, while higher-income years can make that same decision more expensive.

- Retirement timing: The period between when earned income ends and when taxable Social Security income or IRA required minimum distribution (RMD) income begins can look very different from a tax standpoint.

- The mix of accounts available: The balance between pre-tax and after-tax assets influences how withdrawals can be managed later, which in turn affects the role a Roth IRA can play.

The interaction of all of these factors is what makes the strategy complex. A decision made in one year can affect the range of options available in the next.

The same conversion can lead to different outcomes depending on how your income is structured, how it changes over time, and how withdrawals are expected to be handled later. That’s why this isn’t a decision to be made without a full understanding of the greater picture.

Key Rules and Considerations Around Roth IRA Conversions

There are a few baseline rules that all impact how Roth IRA conversions work in practice. They don’t determine whether a conversion makes sense on their own, but they do set the parameters around how the decision can play out.

Here are a few of the more relevant considerations:

- No income limit for conversions: Unlike Roth IRA contributions, eligibility to convert from a traditional IRA isn’t restricted by your overall income. This is one of the reasons conversions are often part of planning discussions for higher-income households.

- The conversion is treated as taxable income: The amount converted is included in ordinary income for the year, which can influence tax brackets and how other income is taxed alongside it.

- No early withdrawal penalty on the conversion itself: Even if the conversion occurs before age 59½, the transaction is not subject to the 10% early withdrawal penalty. The tax impact still applies, however.

- The five-year rule: Converted funds are generally subject to a holding period before certain withdrawals are treated as fully qualified. The details can vary depending on timing and age, but it’s another factor that can affect how and when those assets are used.

These considerations define the conditions under which a conversion takes place, and influence how much flexibility exists in structuring it.

When a Roth Conversion Can Make Sense

There isn’t a single set of conditions that determines whether a Roth conversion is appropriate for your situation or not. In practice, certain situations tend to make the decision more effective, particularly when timing and tax exposure can be managed more deliberately.

Lower-Income Years Create Opportunity

A period of lower income tends to create more flexibility around a conversion. This can happen in the years following retirement but before Social Security begins, during a career transition, or in any gap between higher-earning periods.

In those windows, a traditional IRA to Roth IRA conversion may be taxed at a lower rate than it would be later, which can change the overall outcome.

Future Income May Be Higher

Expectations around future income also factor in. If income is likely to increase over time — whether from required minimum distributions, portfolio withdrawals, or other sources — recognizing some of that income earlier can help manage how it’s taxed across different years.

Flexibility in How Income Is Used

A Roth IRA introduces an added layer of flexibility. Because qualified withdrawals aren’t subject to income tax and there are no required minimum distributions, Roth assets can be used more selectively. That can make it easier to adjust withdrawals over time, particularly when multiple income sources are involved.

Longer-Term Planning Considerations

In some cases, the decision on whether a Roth conversion fits your plan is influenced by how assets are expected to be used over a longer horizon. Roth assets are generally passed to beneficiaries without income tax, which can be relevant in multi-generational planning or when thinking about how assets will be distributed over time.

These factors don’t operate independently; their impact depends on how they align in a given year and how the surrounding decisions are structured.

When a Roth Conversion May Not Be a Fit

There are also situations where a Roth conversion may be less effective, particularly when the immediate cost outweighs the longer-term benefit, or when the surrounding factors don’t support it.

High Immediate Tax Cost

A larger conversion increases taxable income in the year it occurs. If that pushes income into a higher bracket or triggers additional tax considerations, it can limit the efficiency of the decision. Without a clear way to manage how that income is recognized, the upfront cost can be more significant than initially intended.

Shorter Time Horizon

Time plays a role in how a conversion unfolds within your financial situation. If withdrawals are expected sooner rather than later, there may be less opportunity for the tax-free treatment of Roth assets to offset the taxes paid at conversion.

In those cases, the benefit of altering the timing of income can be more limited.

Lower Expected Future Tax Rate

A conversion is often evaluated based on how current tax rates compare to future ones. If income is expected to be meaningfully lower in retirement, whether due to reduced withdrawals or fewer required distributions, the advantage of recognizing income earlier may be less compelling.

When Considered in Isolation

Some of the more important factors aren’t always visible in the initial decision. Social Security taxation, Medicare-related IRMAA thresholds, and other income sources can all be affected by a conversion.

When those elements aren’t accounted for in conjunction, the outcome may look different once everything is considered together.

How Roth IRA Conversions Can Affect Taxes

The tax treatment of a Roth conversion is relatively direct, but its impact depends on the rest of your taxable income.

When you complete a conversion, the amount moved from a traditional IRA is included in ordinary income for that year. It doesn’t get its own separate treatment, but it’s added on top of whatever income is already being recognized — whether from salary, investments, or other sources.

As income increases, it can move into higher marginal tax brackets, which changes how each additional dollar is taxed. Depending on the amount converted, that can be gradual or more pronounced.

And this doesn’t just apply to federal income taxes.

Higher reported income can affect how Social Security benefits are taxed, how Medicare premiums are calculated, and whether certain thresholds tied to deductions or credits are reached. These effects don’t always come up immediately, but they can influence how income is managed across multiple years.

This is why Roth IRA conversion taxes are best evaluated in context with a trusted fiduciary financial advisor.

The tax cost of a Roth conversion isn’t just the dollar amount owed in the year it takes place. Rather, it’s how that income interacts with everything else being reported, and how those interactions carry through into other planning decisions.

How Roth Conversions Are Structured Over Time

Roth conversions should not be approached as a single, one-time decision. The structure behind them tends to carry more weight than any single conversion.

In practice, that often means:

- Recognizing income gradually rather than all at once, so tax exposure can be managed year by year.

- Using available space within a given tax range to determine how much to convert in a specific year.

- Adjusting based on changes in income, whether from work, portfolio withdrawals, or other sources.

- Positioning conversions around key transitions, such as the years before Social Security begins or before required minimum distributions start.

Each of these decisions builds on the last. The amount converted in one year affects the income recognized, the remaining pre-tax balance, and the flexibility available in the next. Over time, that sequence affects how the rest of the strategy plays out.

Because of that, conversions are structured as a series of decisions, where timing, income, and account balances are considered together from one year to the next.

Is a Roth IRA Conversion Right for You?

Both traditional and Roth accounts play their roles in retirement planning. Each offers a different way to manage how and when income is taxed, and the balance between them often shapes how withdrawals can be structured over time.

A traditional IRA to Roth IRA conversion can be a useful tool within that mix, but its value depends on how it’s applied — specifically, how the timing of income recognition fits within the rest of the plan.

That’s why at Towerpoint Wealth, conversions are always considered as part of a broader approach to managing income over time, rather than as a one-time adjustment.

If you’d like to look at how a Roth conversion fits within your own plan, we’re always available as a resource. We invite you to schedule a complimentary 20-minute “Ask Anything” conversation with our team, where we can see how a Roth conversion may or may not be a tool in your overall strategy.

And if someone in your network is working through a similar decision, this may be helpful to pass along. These are often the moments where a more coordinated approach can make a meaningful difference in the long run.