For many households approaching retirement, especially those with higher incomes, Social Security is often viewed as a relatively small piece of the overall financial picture. Investors who have spent decades building substantial portfolios, businesses, or other income-producing assets may assume their Social Security benefit will play only a minor role in supporting retirement.

And, in terms of percentage of income, that may be true. For many Social Security retirees with significant income potential, the benefit itself may represent a modest portion of total retirement income.

Yet the decisions surrounding Social Security still carry meaningful implications.

Claim timing and coordination with other income sources can influence:

- Tax exposure, particularly when retirement income comes from multiple sources.

- The sequencing of portfolio withdrawals.

- Income stability for a surviving spouse.

- How retirement cash flow evolves over time.

In other words, the importance of Social Security for higher-income households tends to lie less in the size of the benefit and more in how it interacts with the broader retirement plan.

For more affluent retirees, Social Security frequently functions as a strategic component of retirement income planning rather than a primary income source. When coordinated thoughtfully with other assets, the timing and structure of benefits can help support longer-term flexibility and income stability.

Before exploring those decisions in more detail, it’s helpful to first understand when retirees typically begin collecting Social Security benefits — and how that choice shapes the options available later on.

When Do Retirees Begin Collecting Social Security?

One of the most common questions Social Security retirees ask is: "What is the best age to apply for Social Security?”

While the answer heavily depends on individual circumstances, the framework itself is straightforward. Retirees generally have three main windows for claiming benefits:

- Early eligibility (age 62): Benefits can begin as early as age 62, but are permanently reduced to reflect the longer expected payout period.

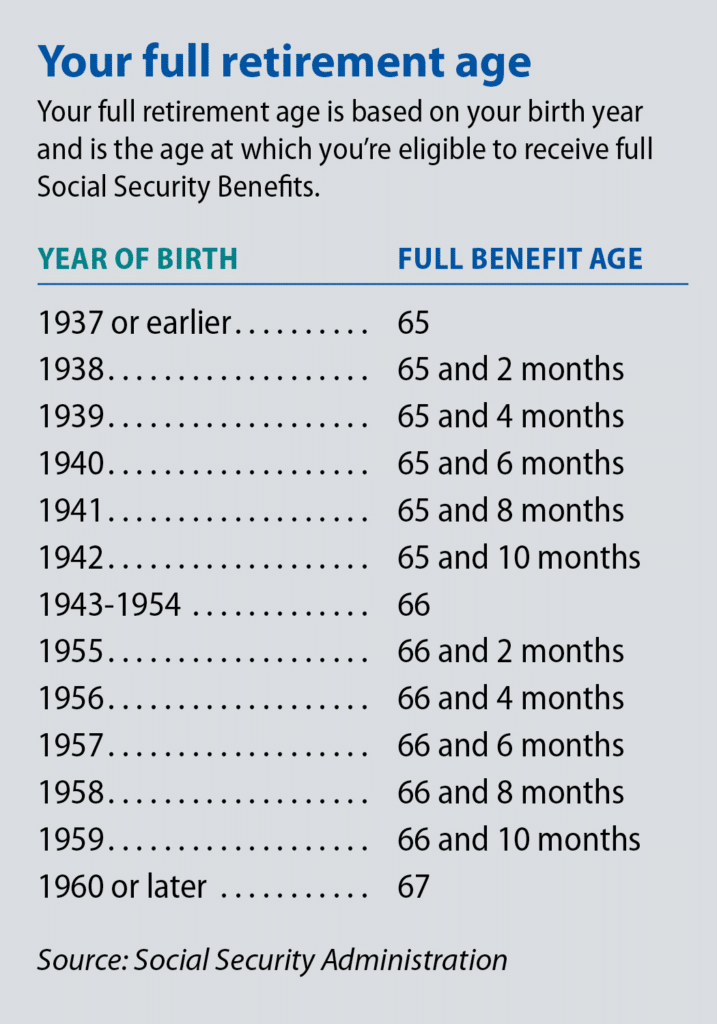

- Full retirement age (typically age 67): This age range is the point at which retirees are eligible to receive their full calculated benefit, based on their earnings history.

- Delayed claiming (up to age 70): For each year benefits are delayed beyond full retirement age, the monthly benefit increases through delayed retirement credits, up until you are age 70.

At a high level, claiming earlier can give you access to income sooner, while delaying increases the amount you may receive later. It’s important to keep in mind that the trade-off here is permanent — once benefits begin, the election is irreversible.

For many retirees, this decision is often framed as a question of maximizing the monthly benefit. In practice, however, the choice is much more nuanced.

Claim timing doesn’t operate in isolation. It interacts with all of the other elements of retirement income, like your portfolio withdrawals, tax exposure, and overall cash flow needs. As a result, the decision is usually less about selecting a single “right” age to claim, and more about how Social Security fits within the broader structure of your retirement plan.

Why Social Security Decisions Can Be More Complex for High-Income Retirees

For higher-income households, Social Security decisions often carry their own breed of complexity.

The benefit itself may represent a smaller share of total income, but it doesn’t work in isolation. Instead, it’s only one component within a broader financial picture that may include:

- Taxable investment income

- Withdrawals from retirement accounts

- Real estate income

- Business distributions

- Pensions or deferred compensation

Each of these income sources has its own characteristics, timing, and tax treatment. When combined, they create a layered structure where the introduction of Social Security can influence more than just monthly cash flow.

For many retirees, this is where Social Security retirement planning is much more nuanced than meets the eye. The timing of benefits can affect:

- How total income is recognized from year to year

- How different income sources are coordinated

- How much flexibility remains in managing withdrawals over time

When it comes to Social Security for high-income earners, the interaction of all of these “levers” is particularly relevant. Even though the benefit may be modest (relative to your overall assets), the timing of when it begins can influence how other income sources are taxed and how your retirement income is structured.

How Claiming Social Security Affects Taxes

The question that often follows claim timing is: “When does Social Security income become taxable?”

The answer depends on how Social Security interacts with other sources of income within a broader Social Security retirement planning framework. Benefits are evaluated using a measure commonly referred to as combined (or provisional) income, which includes:

- a portion of Social Security benefits

- taxable income from investments or retirement accounts

- certain other income sources

As total income rises, a greater portion of Social Security benefits may be subject to federal income tax. For many higher-income retirees, this can mean that up to 85% of benefits become taxable.

This is where you can truly see how the interaction between income sources affects Social Security decisions, even if it’s a relatively small income source in your retirement plan. For households with multiple income streams, the timing of when benefits begin can influence:

- The overall taxable income in a given year

- How and when retirement account withdrawals are taken

- The realization of capital gains from investment portfolios

- Medicare premium brackets, which are tied to income levels

In the greater context of your financial life, Social Security is a moving piece that often best serves in a coordinated and tax-efficient financial and retirement income plan.

The Role of Claim Timing in a Social Security Claiming Strategy

At a high level, retirees typically evaluate the three aforementioned timing paths when it comes to Social Security. Each comes with its own trade-offs, particularly for households with higher incomes and multiple financial priorities.

Claiming Early

Beginning benefits at age 62 provides earlier access to income, which can be appealing for retirees looking to reduce reliance on portfolio withdrawals in the early years.

However, that decision comes with VERY important trade-offs:

- The monthly benefit is permanently reduced.

- Future cost-of-living adjustments are applied to a lower base.

- Survivor benefits may also be lower, which can affect a spouse’s longer-term income.

Waiting Until Full Retirement Age

Claiming at full retirement age offers retirees a more balanced approach.

At this point, retirees receive their full calculated benefit, without early reductions or delayed credits. For some, this timing aligns naturally with retirement income needs and simplifies coordination with other sources of income.

Delaying Benefits

Delaying Social Security beyond full retirement age increases the monthly benefit through delayed retirement credits, up to age 70.

For higher-income retirees, this can offer several advantages, such as:

- A larger lifetime benefit, particularly for those with longer life expectancies

- A higher survivor benefit, which can play a meaningful role in longer-term planning

- An additional layer of longevity protection, helping support income later in retirement

In this context, delaying Social Security is not simply about increasing a monthly payment. For many households, it actually functions as a form of income durability, providing a stable, inflation-adjusted stream that continues regardless of market conditions.

That said, there is no single “correct” claiming age. The decision depends on how Social Security integrates with other income sources, tax considerations, and longer-term goals.

How Social Security Claiming Decisions Affect Survivor Benefits

A question that often receives less attention than overall timing is how delaying Social Security affects survivor benefits. For married couples, this is a consideration that plays a meaningful role in the decisions that follow.

In most cases, when one spouse passes away, the surviving spouse receives the larger of the two Social Security benefits. As a result, the timing decision made by the higher-earning spouse can directly influence the level of income available later on.

Delaying benefits increases the retiree’s own monthly benefit while also increasing the eventual survivor benefit that a spouse may rely on. For this reason, your individual Social Security decisions are often better viewed as household decisions, rather than individual ones.

Even for couples with significant assets, Social Security can still serve an integral role in a broader financial plan. It provides a stable, inflation-adjusted income stream that continues regardless of market conditions — which can be especially valuable for a surviving spouse managing the next phase of retirement.

In this sense, the value of delaying benefits is not limited to the years both spouses are living. It can extend well beyond that, supporting income continuity over a potentially longer time horizon.

Coordinating Social Security Within a Broader Retirement Strategy

As we’ve discussed in the earlier sections, Social Security decisions don’t typically stand on their own.

For higher-income households, the timing of benefits becomes one part of a much larger conversation that includes:

- IRA withdrawals and required distributions

- Taxable investment income

- Roth conversion considerations

- Ongoing portfolio withdrawals

Each of these elements will influence how your income looks over time. When Social Security is introduced into that mix, it can change not only total income, but how that income is taxed, how it is sequenced, and how flexible a plan remains in different market environments.

In some cases, retirees use the years leading up to claiming benefits to:

- Manage how income is recognized from year to year

- Evaluate when and where withdrawals are taken

- Consider how different income sources interact over time

At Towerpoint Wealth, we view these decisions through a broader lens and work with you to coordinate all aspects of your financial life. When these elements are considered together, Social Security can serve less to maximize a single benefit and more to support a cohesive, well-structured retirement plan.

Working with a trusted fiduciary financial advisor can help bring that structure into focus to maximize results to support your unique situation. Rather than evaluating each decision in isolation, the process centers on understanding how income, taxes, and longer-term goals interact — and how those relationships evolve over time.

Ultimately, this kind of coordination helps ensure that Social Security decisions support not just a moment in time, but the overall direction of your financial life.

Why Thoughtful Social Security Decisions Matter

For many Social Security retirees, the benefit itself may represent only one piece of the overall financial picture. This tends to be the case especially with households that have more assets in accounts for retirement.

But the decisions surrounding Social Security can have a broader impact than many people expect, and the wrong decisions can be costly if not properly evaluated.

Claim timing can influence:

- Retirement income stability over time

- Tax outcomes, particularly when multiple income sources are involved

- Survivor benefits and long-term income continuity

- Flexibility in how income is managed throughout retirement

The most effective Social Security claiming strategies rarely ever come from focusing on one variable in isolation, as is the case with most longer-term financial decisions. They come from stepping back and evaluating how benefits interact with your income, taxes, and longer-term priorities.

If you’d like to see how these decisions fit into your broader retirement income strategy, we invite you to schedule a complimentary 20-minute “Ask Anything” conversation with our team.

It’s an opportunity to walk through your questions and gain clarity on how Social Security decisions and coordination across all aspects of your financial life can support the next phase of your life.