For many higher-income filers, the decision between the standard deduction vs. itemized deduction can feel almost automatic. The standard deduction has increased significantly in recent years, and as a result, fewer households find themselves itemizing the way they once did.

On the surface, it seems like this would simplify tax season. But in practice, it has simply changed where thoughtful tax planning shows up.

Taking the standard deduction doesn’t mean tax planning disappears. It just means the conversation moves from deciding what to deduct toward understanding how income, investments, and longer-term decisions interact over time.

That’s the perspective we want to share in this article. At Towerpoint Wealth, we don’t believe tax planning is about trying to make the “perfect” deduction decisions or chasing tax strategies with a narrow focus on one figure.

Instead, it’s about revisiting what still matters once the standard deduction is likely in play — and how tax season planning can serve as a moment to step back and evaluate whether your broader financial picture remains in line with your goals.

Before looking at the areas that often deserve attention, it helps to revisit what actually separates the standard deduction from itemizing in the first place.

Standard Deduction vs. Itemizing: A Decision Simpler Than It Used to Be?

At its core, the difference between the standard deduction vs. itemized deductions is relatively straightforward.

The standard deduction provides a fixed dollar amount that reduces your taxable income. Itemizing, on the other hand, means listing eligible expenses individually — things like mortgage interest, certain taxes, charitable contributions, and other qualifying deductions.

In the past, many higher-income households routinely itemized. But thanks to changes in tax law — including limits on mortgage interest and state and local tax deductions, along with a significantly higher standard deduction — the math often looks different.

Today, for many filers, the decision itself is more straightforward than it used to be. The standard deduction often becomes the default simply because the sum of fewer tax-deductible expenses does not exceed the “itemization threshold.”

But this is where an important misconception shows up: while the filing choice to take the standard deduction may be simpler, tax planning itself hasn’t necessarily become less complex. In many cases, it has just changed.

And that leads to the more interesting question — what still deserves “tax attention” when itemizing is no longer the driver of the conversation?

What Changes If the Standard Deduction Becomes the Default

One of the more common assumptions we see during tax season planning is that once the standard deduction becomes the obvious choice, there’s less left to think about.

If itemizing isn’t on the table anymore, it can feel like most of the planning decisions have already been made. In reality, that’s usually not what’s happening. The planning doesn’t disappear — it just looks different.

When itemized deductions no longer drive the conversation, the focus often moves away from tracking deductible expenses, and toward how income is structured and coordinated instead. The timing of withdrawals, the mix of income sources, and how different decisions interact throughout the year begin to matter more than the deduction itself.

In other words, the question changes, but it still needs to be answered.

It becomes less about maximizing deductions and more about understanding how the broader financial picture influences your taxable income over time. Filing decisions still matter — but they’re only one piece of a much bigger system that still needs planning.

That shift in perspective is important because it opens the door to the opportunities where thoughtful planning can still make a meaningful difference — even if the standard deduction is the default.

Often-Overlooked Areas That Still Matter When You Claim the Standard Deduction

Choosing the standard deduction can make filing feel simpler — but it doesn’t eliminate the places where thoughtful tax season planning still matters. In many cases, the focus moves away from deductions and instead narrows in on how financial decisions are structured over time.

Charitable Giving Still Plays a Role

Even when itemizing isn’t part of the equation, charitable giving remains closely tied to broader financial planning. For many households, the conversation now can become less about the immediate deduction and more about how giving aligns with longer-term goals, timing, and overall cash flow.

In other words, the tax outcome may no longer be the primary driver (though still in the car), but the planning considerations around generosity and intention are still very relevant.

Recent legislation further supports charitable giving and its role in tax planning. Beginning in 2026, provisions within the “One Big Beautiful Bill Act” (OBBBA) introduce several changes worth understanding:

Key charitable giving considerations for 2026 include:

- Above-the-line deductions for non-itemizers: Taxpayers claiming the standard deduction may deduct up to $1,000 (single-filers) or $2,000 (married filing jointly) for qualifying cash donations. Donor-advised funds (DAFs) are excluded.

- A new AGI threshold for itemizers: Charitable deductions generally apply only to contributions exceeding 0.5% of adjusted gross income, potentially changing how larger gifts are evaluated.

- Limits for higher-income donors: The maximum tax benefit for charitable deductions may be capped at 35%, which can influence how philanthropy fits into broader tax planning discussions.

Rather than changing the motivation behind giving, these updates further highlight why charitable decisions are best viewed within a larger planning framework. Tax rules may shift from year to year, but thoughtful coordination helps ensure generosity remains aligned with longer-term priorities.

Family-Focused Tax Credits and Education Planning

Several credits tied to family and education decisions exist outside the itemized deduction discussion altogether. Depending on income levels and eligibility rules, households may still encounter credits such as:

- the child tax credit and related family-focused credits

- the child and dependent care credit

- the adoption credit

- education-related credits like the American Opportunity Credit or the Lifetime Learning Credit

For many higher-income households, phase-outs mean these benefits may be reduced or unavailable — but they’re still important to understand, especially in years where income changes or family circumstances evolve.

Education Debt and Early-Career Support

Some families continue supporting younger adult children or helping with education costs well beyond college. While deductions like the student loan interest deduction are often limited by income thresholds, they remain part of the broader conversation when planning across generations.

Retirement Contributions and Above-the-Line Adjustments

Some tax breaks for high-income earners operate independently of whether a return is itemized. Pre-tax retirement contributions and certain adjustments to income can continue to influence taxable income while also shaping longer-term flexibility.

This is a good reminder that the standard deduction doesn’t close the door on tax-aware decision-making; it just changes where those decisions live.

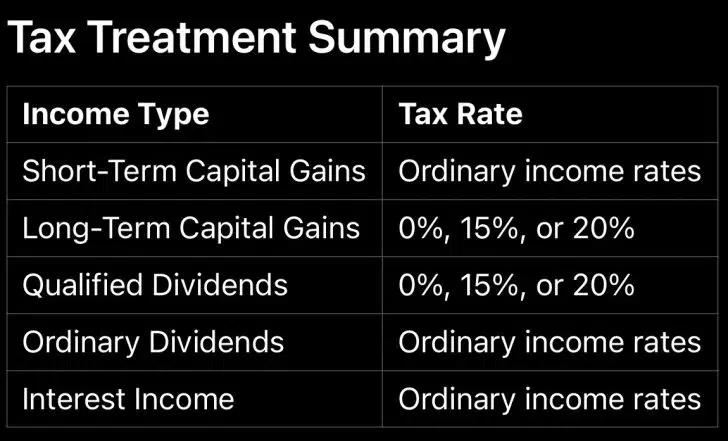

Investment Income and Tax Character

Investment income is another area that doesn’t change just because deductions are simplified. Dividends, interest, and capital gains each carry their own tax treatment, and how income is generated within a portfolio can influence outcomes from year to year.

Multi-Year Planning Considerations

Some households naturally find that their filing approach changes from one year to the next. There may be years when the standard deduction makes the most sense and others when itemizing stands out as the winner.

The point isn’t to force one approach or the other, but to recognize that tax decisions often unfold across multiple years rather than in isolation. Looking at the bigger picture can help avoid overly-narrow thinking during any single filing season.

State and Federal Differences

While federal filing may feel straightforward, state tax rules don’t always follow the same framework. Differences between state and federal treatment can create outcomes that aren’t immediately obvious when focusing only on a federal return.

For households with more complex income or multiple residences, the distinction between the two can shape the bigger picture.

Why This Matters More for Higher-Income Filers

What tends to add complexity for higher-income households is the structure of income, not the standard vs. itemized deduction debate.

Multiple income sources often begin to overlap: investment income alongside retirement account activity, business or consulting income, equity compensation, or other forms of variable earnings.

Each category may be taxed differently, and the interaction between them can influence outcomes in ways that aren’t immediately obvious during filing season.

Investment income adds its own layer. Dividends, capital gains, and interest don’t rely on itemized deductions to create tax impact. Their timing and character can shape overall taxable income, which in turn can affect planning decisions elsewhere.

For some households, equity compensation or business-related income introduces additional considerations. These income sources may fluctuate year to year, creating periods where tax outcomes look very different even when lifestyle spending remains relatively steady.

And that’s where the bigger planning conversation begins. The decisions that matter most often center around a holistic view of taxes, investment strategy, and longer-term goals — not the deduction line itself.

At Towerpoint, we often see that complexity doesn’t come from deductions alone. More often, it comes from how income is structured, how it evolves over time, and how each piece fits into the broader financial picture.

From “Deduction Strategy” to Planning Strategy

When clients sit down with us during tax season, the conversation rarely starts with deductions alone. Instead, we begin by looking at how income flows through the broader plan.

That means understanding how cash flow decisions, investment strategy, and retirement planning intersect — and how those moving parts influence one another from year to year. Taxes are part of the discussion, but they’re always considered within a bigger framework rather than as a standalone objective.

At Towerpoint, this often involves coordinating with a client’s CPA or tax professional to ensure investment decisions, income sources, and longer-term goals remain aligned. This is not to make reactive adjustments during filing season, but to confirm that the overall structure still makes sense as circumstances evolve.

When tax planning for high-income earners is viewed this way, filing season becomes less about finding last-minute opportunities and more about reinforcing decisions that support stability and flexibility over time.

Final Thoughts

Choosing the standard deduction can make filing feel more straightforward, but it doesn’t mean the planning conversation stops there.

Tax season is rarely just about reducing this year’s bill. More often, it’s an opportunity to step back and look at how income decisions, investment strategies, and longer-term goals work together. The mechanics of filing may feel simpler, but the bigger picture still deserves attention.

In many cases, the most meaningful insight is recognizing how ongoing decisions shape flexibility and outcomes over time. Planning continues, even when the tax return itself feels easier.

At Towerpoint Wealth, we believe the strongest high-income-earner tax strategies come from seeing how all the pieces connect — not just during tax season, but year-round.If you’d like help reviewing how your tax decisions fit into your broader financial plan, we invite you to schedule a 20-minute complimentary conversation with our team. Sometimes a thoughtful review is all it takes to move forward with greater confidence.