Tax season is here, and if you’re an investor, that means there’s something that should be on your radar — 1099 forms. Whether you’ve earned interest from bonds, dividends from stocks, or capital gains from your trading activity, the IRS wants to know about it.

But, when done strategically, tax reporting isn’t just about compliance; it’s an opportunity to optimize your investment strategy and minimize unnecessary tax burdens.

Understanding what is on a 1099 tax form and how to use it to your advantage is key to protecting your wealth. Misreporting gains, overlooking deductions, or misunderstanding tax rates could leave you paying more than you need to — or worse, trigger unwanted IRS scrutiny.

For investors managing complex portfolios, tax planning isn’t something to think about once a year. It’s a year-round strategy that can help preserve more of your returns and keep your portfolio working efficiently.

In this article, we’ll walk through:

- The different types of 1099 forms investors receive and what they mean for your taxes.

- How to interpret your brokerage 1099 and avoid common tax pitfalls.

- Key strategies to reduce tax liability and improve portfolio efficiency.

The U.S. tax code is complicated, but navigating it doesn’t have to be. With the right knowledge, the right financial and tax advisor, and a proactive plan, you can make tax season another opportunity to strengthen your longer-term financial strategy.

What is a 1099 Tax Form?

If you’ve earned investment income in a non-retirement, “taxable” account, you may be wondering: What is a 1099, and how does it impact my tax return?

A 1099 tax form is one of the most common documents investors receive during tax season. It’s how brokerage firms, banks, and other financial institutions report taxable income to both you and the IRS.

Unlike a traditional W-2, which reports income from an employer, a 1099 tracks investment-related income — including dividends, interest, and capital gains — that isn’t subject to automatic withholding.

For investors, understanding what’s on a 1099 is essential. If you’ve earned interest from a high-yield savings account, received dividends from stocks, or sold assets for a gain, these transactions need to be reported correctly to avoid unnecessary tax liabilities.

Types of 1099 Forms Investors Need to Know

If you’re an investor, chances are you’ll receive at least one 1099 tax form during tax season. Depending on the types of investments you hold and the transactions you’ve made throughout the year, your brokerage firm may issue multiple forms, each reporting a different type of income.

Investors must understand the different types of 1099 forms because not all 1099 income is taxed the same way.

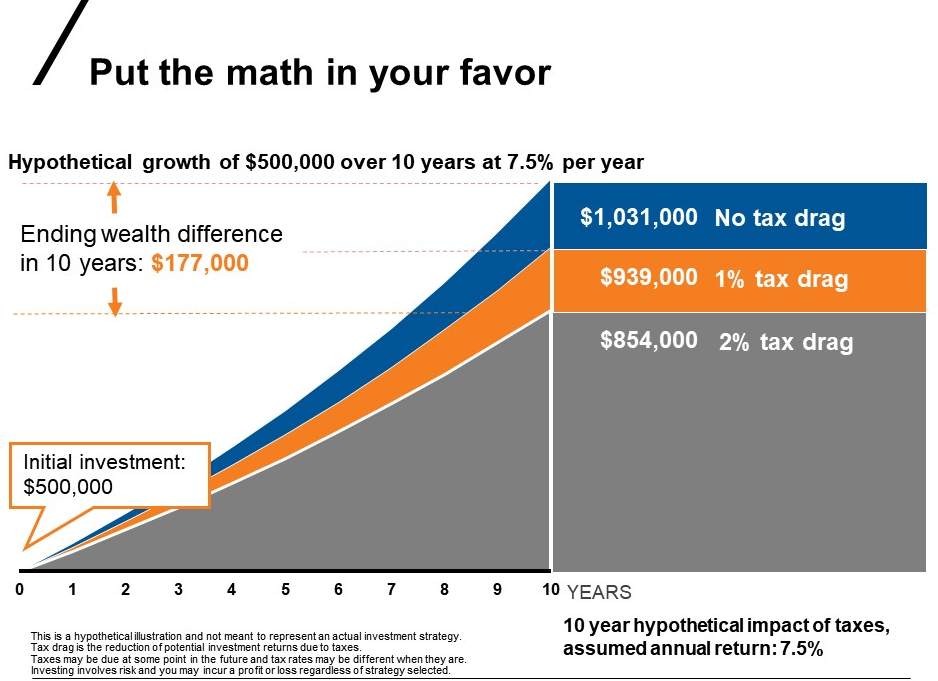

Qualified dividends, for example, may be taxed at a lower federal rate (usually 15%) than ordinary income, while short-term capital gains (from assets held less than a year) are taxed at a higher rate than long-term capital gains. Understanding these distinctions is critical to properly managing your tax liability and ensuring your investment strategy is as tax-efficient as possible.

Failing to report 1099 income accurately can lead to IRS penalties or an unexpected tax bill. Since your brokerage firm sends a copy of your 1099 to the IRS, any discrepancies could raise red flags and result in additional scrutiny.

Understanding these forms — and how they impact your tax liability — is essential for effective tax planning and portfolio efficiency.

1099-INT: Reporting Interest Income

The IRS 1099-INT form is issued when you earn more than $10 in interest income from bank accounts, bonds, or money market funds. While this may seem straightforward, the tax treatment of interest income varies depending on the source.

- Taxable Interest – Interest earned from savings accounts, corporate bonds, and certificates of deposit (CDs) is taxed as ordinary income, meaning it is subject to your highest marginal tax rate.

- Tax-Exempt Interest – Interest earned from municipal bonds is generally exempt from federal taxes and may also be exempt from state and local taxes, depending on where the bond was issued.

- U.S. Treasury Interest – Interest from Treasury bonds, bills, and notes is exempt from state and local taxes but still subject to federal taxes.

For investors who hold fixed-income securities, understanding how 1099-INT income is taxed is key to structuring a tax-efficient portfolio and preparing for tax season.

1099-DIV: Reporting Dividend Income

If you received $10 or more in dividends, your brokerage will issue a 1099-DIV form. This form reports dividends and capital gain distributions from stocks, ETFs, and mutual funds. However, not all dividends are taxed the same way.

- Qualified Dividends – These dividends are taxed at long-term capital gains rates (0%, 15%, or 20%, depending on your taxable income). To qualify for this favorable tax treatment, the stock must meet specific requirements, as determined by the IRS.

- Nonqualified Dividends – Also known as ordinary dividends, these are taxed as ordinary income, meaning they could push you into a higher tax bracket.

- Capital Gains Distributions – If you own mutual funds or ETFs, you may receive capital gains distributions, which occur when the fund manager sells securities within the fund. These are taxed based on whether they are short-term or long-term gains, even if you didn’t sell shares yourself.

For investors looking to manage their tax liability, placing dividend-generating investments in tax-advantaged accounts such as IRAs or Roth IRAs can help reduce tax exposure over time.

1099-B: Reporting Stock and Asset Sales

If you sold investments — such as stocks, bonds, mutual funds, or ETFs — you’ll receive a 1099-B from your brokerage. This form reports:

- Proceeds from sales.

- Cost basis (what you originally paid for the investment).

- Short-term vs. long-term classification.

The difference between the sale price and your cost basis determines whether you have a capital gain or loss. Short-term capital gains (held less than one year) are taxed at ordinary income rates, which can be as high as 37%, depending on your income.

On the other hand, long-term capital gains (held more than one year) are taxed at the more favorable capital gains tax rates (0%, 15%, or 20%).

Key Tax Considerations for Investors:

- Wash Sale Rules – If you sell a security at a loss and repurchase a “substantially identical” asset within 30 days, you cannot claim the loss for tax purposes. This can impact tax-loss harvesting strategies.

- Missing Cost Basis – Some brokerage firms may not provide cost basis details for older investments. If the cost basis is not included, you may be taxed on the full proceeds of a sale unless you have accurate records.

1099-MISC: Reporting Miscellaneous Investment Income

A 1099-MISC is less common for stock market investors, but may apply if you earned:

- Rental income from investment properties.

- Royalties from intellectual property or mineral rights.

- Certain alternative investment earnings.

Unlike other investment-related 1099 forms, a 1099-MISC reports miscellaneous income, such as rental earnings or royalties. Investors receiving this form should follow the IRS 1099-MISC form instructions carefully to ensure they properly report income and avoid self-employment tax surprises.

1099-R: Reporting Retirement Account Distributions

If you have taken withdrawals from a 401(k), IRA, pension, or annuity, your financial institution will issue a 1099-R to report the distribution. A 1099-R can be issued regardless of whether the distribution is taxable. For example, when you roll over retirement assets directly from a 401(k) to an IRA, you will receive a 1099-R for the rollover — even though this is not a taxable event.

- Traditional IRA and 401(k) withdrawals are taxed as ordinary income.

- Roth IRA withdrawals are tax-free, provided you meet the IRS’s eligibility requirements.

- Early withdrawals (before age 59½) may trigger a 10% penalty in addition to ordinary income taxes unless an exception applies.

- Required Minimum Distributions (RMDs) from tax-deferred accounts begin at age 73 and must be reported on your tax return.

- Direct rollovers or rollovers processed within 60 days from one qualified account to another qualified account are non-taxable events.