By: Steve Pitchford, Director of Tax and Financial Planning and Matt Regan, Wealth Advisor

Published: April 13, 2021 updated October 22, 2021

Most individuals who are philanthropically inclined usually just take the path of least resistance and write a check directly to a charity. Of course, this is a straightforward approach and can qualify for an income tax deduction, but when being charitable, there are many different (and often economically more advantageous) options and strategies available to you. Indeed, with strategic and thoughtful planning, a taxpayer may be able to optimize their gifting strategy, meeting multiple objectives by maximizing the economic benefits 1.) to themselves, 2.) to their favorite charities, and even 3.) to their loved ones.

Are you optimizing your philanthropy and gifting strategy? Below you will find a myriad of different charitable strategies we regularly employ for Towerpoint Wealth clients, designed to help you better understand your options.

Cash/Direct to Charity

A cash gift is the simplest and (by far) most popular form of charitable giving.

The income tax deduction[1] for a cash gift is generally equal to the amount of cash donated less the value of any goods or services received in return. And while the benefit of a cash donation is its simplicity, as you will see below, it is not always optimal from a tax and gifting perspective.

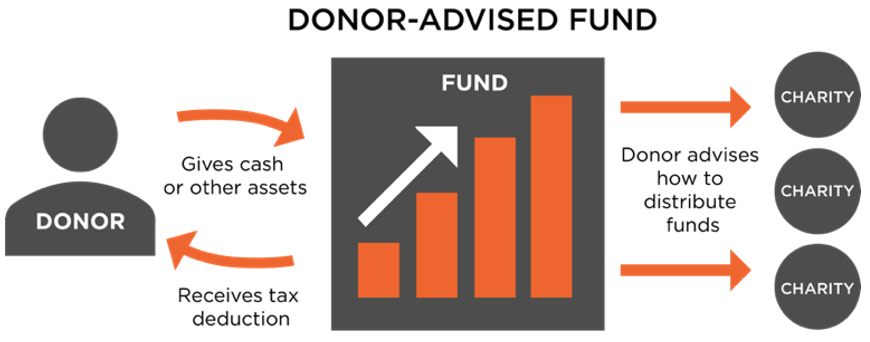

Donor-Advised Fund

A Donor-Advised Fund (DAF) is a charitable fund, a 501(c)(3) entity in and of itself, that allows an individual to donate cash or appreciated securities, such as individual stocks, bonds, mutual funds, or exchange-traded funds (ETFs).[2]

Donating appreciated securities can be a more tax advantageous way to fund a DAF, as donating an investment that has gone up in value generally provides the exact same tax deduction as donating cash, while at the same time provides the extra benefit of eliminating the capital gains tax that a taxpayer would normally pay upon selling the security.

How does it work? The donor makes an irrevocable gift of cash or appreciated securities to a DAF. The donor is then able to decide, on their own timeline, when to grant funds out of the DAF and directly to a charity or charities of their choice. If the contribution is appreciated securities, the DAF is allowed to sell these positions tax-free. The DAF will typically then, at the donor’s discretion, invest the funds in a manner consistent with the donor’s charitable goals and objectives. Once the donor is ready to make a grant from the DAF, he or she simply informs and authorizes the DAF custodian (usually via the custodian’s online platform) to send a check directly to the charity on the donor’s behalf.

Typically, the funding and operational costs of DAFs are low, and our clients also love that they provide a year-end summary report, eliminating the hassle and stress of tracking each contribution/grant out of the DAF individually.

Towerpoint Tip:

At Towerpoint Wealth, we also evaluate “frontloading” a DAF with several years’ worth of potential charitable contributions, allowing a taxpayer to “hurdle” the standard deduction and thus, not only eliminate the future capital gains tax of the donated funds, but also provide them with at least a partial tax deduction for their charitable contributions in a particular tax year.

Private Foundation

A private foundation is a 501(c)(3) organization set up solely for charitable purposes.

A private foundation may be structured either as a corporation managed by a board of directors, or as a trust managed by trustees. Unlike a public charity, the funding for a private foundation typically comes from a single individual, family, or corporation.

The primary benefit of a private foundation is the enhanced control that it provides, as it is able to formulate its own customized charitable gifting approach and platform (and continue to gift directly to other charities as well). A donation to a private foundation is an irrevocable charitable gift, and qualifies for a potential income tax deduction that, for most individuals, will be the exact same as gifting directly to another 501(c)(3) charity.[3]

Importantly, private foundations have administrative and tax reporting requirements that may be costly, and speaking further with a financial advisor and tax professional regarding the benefits and drawbacks of establishing one is recommended.

IRA Qualified Charitable Distribution

Individuals who are over the age of 73 are subject to annual required minimum distributions (RMDs) from their pre-tax IRA(s). These distributions are included on an individual’s tax return as taxable income and are subject to ordinary income tax.

As an alternative to taking a “normal” RMD, an individual can instead execute a Qualified Charitable Distribution (QCD), which allows them to both satisfy their RMD and their charitable intention at the same time.

How does a QCD work? Instead of a “normal” RMD, which usually is deposited into an individual’s checking, savings, or brokerage account, a QCD is paid directly from the IRA to a qualified charity. This distribution not only offsets – or, depending on the amount, fully satisfies – an individual’s RMD, but it is also excluded from taxable income.[4]

And unlike other gifting strategies, a QCD’s net effect as an “above the line” dollar-for-dollar tax deduction can offer additional economic benefits when compared to a “typical” itemized charitable tax deduction.

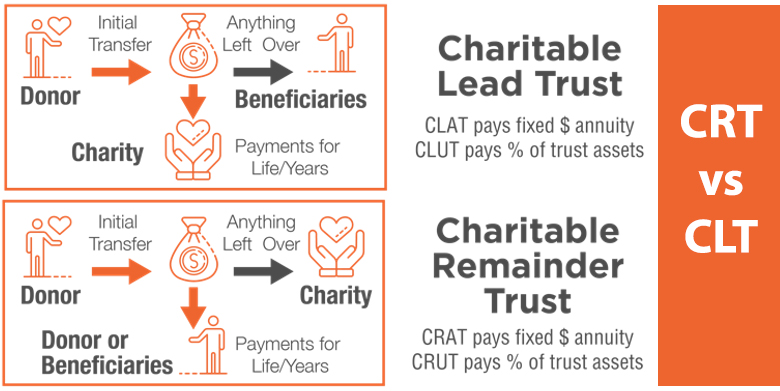

Charitable Remainder Trust

A charitable remainder trust (CRT) allows a donor to make a future charitable gift, while at the same time, receive an income stream during their lifetime for their own spending goals and needs. There are two types of CRTs: Charitable Remainder Annuity Trusts (CRATs) and Charitable Remainder Unitrusts (CRUTs). The two main differences are how the annual distribution to the income beneficiary(ies) is calculated and how often assets can be contributed to the trusts.[5]

When the donor establishes and contributes to a CRT, they are entitled to a current income tax deduction that is equal to the future expected value of the trust assets that will ultimately pass to the charitable beneficiary(ies). The deduction calculation is based on a number of different factors, such as the annual income stream payout set by the CRT, the age(s) of the income beneficiary(ies), the trust’s specified term of years, and the published IRS monthly interest rate.

At either 1.) the donor’s death, 2.) the death of the beneficiary, or 3.) the completion of the trust’s term, the trustee will distribute the balance of the trust assets directly to the chosen charity(ies).

The primary benefit of a CRT is that an individual may receive a substantial tax deduction in the year they open and fund the CRT, while at the same time, continue to receive income for themselves (or other income beneficiaries) during their lifetime. If the CRT is funded with cash, the donor can claim a deduction of up to 60% of adjusted gross income (AGI); if appreciated assets are used to fund the trust, up to 30% of their AGI may be deducted. In addition, if the trustee decides to sell contributed appreciated securities, he or she can do so tax-free.

Towerpoint Tip:

Opening, funding, and administrating a CRT is complicated and there are important ongoing tax filing obligations. As such, it is highly recommended to work with a trusted financial advisor and tax professional to ensure that a CRT is the right choice. Further, the tax deduction calculation may be audited, so it is important to hire a qualified professional to appraise this value.

Charitable Lead Trust

In the simplest sense, a charitable lead trust (CLT) is the reverse of a CRT. The income generated by the contributed assets is distributed to the chosen charity, and the beneficiaries receive the remainder interest. Like a CRT, a CLT can be an annuity trust (CLAT) or a unitrust (CLUT), but different distribution rules apply.

There are two main types of CLTs: a grantor CLT and a non-grantor CLT. A grantor CLT, like a CRT, is designed to give the donor an upfront charitable income tax deduction. However, to receive the charitable deduction, the donor must be willing to be taxed on all trust income. Since the gift is “for the use of” a charity instead of “to” a charity, cash contributions to a grantor CLT are subject to reduced deduction limits of 30% of AGI, and appreciated asset contributions are subject to deduction limits of 20% of AGI. For non-grantor CLTs, the grantor does not receive a charitable income tax deduction, nor are they taxed on the income of the trust. Instead, the trust pays tax on the income, and the trust claims a charitable deduction for the amounts it pays to the charity. It is very important to note that since they are not tax-exempt, neither type of CLT offers the ability to avoid or defer tax on the sale of appreciated assets like a CRT does.

A CLT may be a better option than a CRT if an individual has no need for current income and wants to ensure that, upon their death, their loved ones receive an inheritance.

Towerpoint Tip:

A charitable lead trust is often structured to provide gift-tax benefits, not necessarily a current income tax deduction. A donor is able to gift more to family members with a reduced gift-tax effect because the gift’s present value is discounted by the calculated income to be paid to the charity(ies). The tax deduction the individual receives is based on the annual amount provided to the charity.

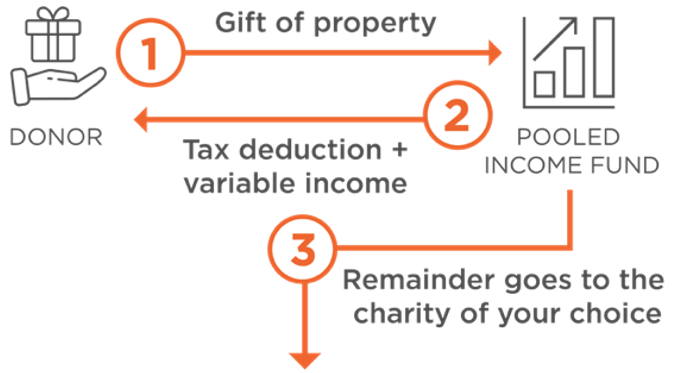

Pooled-Income Fund

A Pooled-Income Fund (PIF) is a type of charitable trust that functions like a mutual fund.

A PIF is comprised of assets from many different donors, pooled and invested together. Each donor is assigned units in the fund that reflect his or her share of the fund's total assets. Each year, the donors are paid their proportionate share of the net income earned by the fund – the distribution amount depends on the fund’s performance and, importantly, is taxable income to the beneficiary (which is typically the donor but may also be a family member, friend, etc.). At the death of each income beneficiary, the charity receives an amount equal to that donor’s share in the fund.

PIF contributions provide a tax deduction to the donor upon contribution and, like the other charitable gifting vehicles described previously, affords the donor the ability to avoid paying any capital gains taxes on the contributed appreciated securities.

A primary drawback of a PIF is that the donor has no control over how the assets are invested, as the investment of the fund is directed by a professional manager. As such, it is important that individuals speak with a financial advisor to ensure that a PIF is thoughtfully incorporated into their overall investment allocation and strategy, as well as philanthropic and charitable giving plan.

How can we help?

At Towerpoint Wealth, we are a legal fiduciary to you, and embrace the professional obligation we have to work 100% in your best interests. If you would like to learn more about charitable giving strategies, we encourage you to contact us to open an objective dialogue.

Have additional questions? Contact our Director of Tax and Financial Planning, Steve Pitchford, for a 20-minute “Ask Anything” meeting.

[1] In order for an individual to receive a tax deduction, their combined itemized deductions must exceed their standard deduction.

[2] Appreciated securities may be donated directly to certain charities as well. However, doing so is typically an administrative hassle for both the individual and the receiving organization.

[3] Donations to a private foundation are tax deductible up to 30% of adjusted gross income (AGI) for cash, and up to 20% of AGI for appreciated securities, with a five-year carry forward

[4] Up to an annual maximum of $100,000, per taxpayer.

[5] A CRAT pays a fixed percentage (at least 5%) of the trust’s initial value every year until the trust terminates. The donor cannot make additional contributions to a CRAT after the initial contribution. A CRUT, by contrast, pays a fixed percentage (at least 5%) of the trust’s value as determined annually. A donor can make additional contributions to a CRUT.