It’s right around the corner, and it isn’t going to be pretty, so let’s discuss the election's impact on the stock market now and get it out of the way.

For a good part of this calendar year, we have counseled you that it is prudent to give advance thought to the range of potential economic, regulatory, taxation, spending, budget deficit, societal, and financial market implications of the national election results, depending on whether Republicans or Democrats win one or more of the White House, the House of Representatives, and the Senate.

After Labor Day, the campaign is likely to reflect increased amounts of political vociferousness, perhaps some degree of vehemence, and even apportionments of vitriol (we hope and pray not too much), with the potential to cause meaningful shorter-term shifts in financial asset prices. That is precisely why we recommend forming beforehand, and sticking to, a well-reasoned and disciplined asset allocation plan and investment strategy tailored to your personal and financial circumstances, time horizon, objectives, and temperament.

November 2020: The 59th Quadrennial Presidential Election

September, October, and then, the Election: With the VIX volatility index (see the Graph of the Week below) having risen an average of four points ahead of each of the last seven presidential elections since this measure was created, important issues to consider in the upcoming weeks ahead include:

- How clearly (and energetically) each political party's convention message was received, perceived by, and responded to by their respective loyal voter bases;

- The nation’s reactions to the anticipated three presidential debates and one vice presidential debate;

- Assessments of the strength of party identification among various segments of the voting population, as well as in the composition of the overall electorate; at the same time, taking into account the ability of each ticket to generate serious backing from less-supportive voter populations;

- Which candidate voters (considering demographic attributes, where they live, how they classify themselves on the political spectrum, and other characteristics) think can better confront America’s broad challenges, including the coronavirus pandemic, the economy, social issues, and pressing global concerns;

- The effectiveness of voting procedures, trust in mail-in balloting, the degree of putative social media and foreign-based election interference, actual voter participation, and the perceived veracity and legitimacy of the results; and

- The potential consequences of prolonged uncertainty associated with a contested election (should it occur) for social order and the financial markets.

Some Implications of Potential Scenarios

Roughly one in five workers are currently receiving jobless benefits, and early expectations of a V-shaped recovery have been hindered by renewed coronavirus outbreaks. Regardless of who wins the 2020 election and in what manner, financial asset valuations appear to be reflecting expectations that whenever the coronavirus pandemic ends, some degree of economic acceleration is likely to take place in the U.S.

As we have counseled for some time, it is important to devote thought and attention to the taxation, regulatory, economic, asset allocation, and investment strategy implications of the three leading potential electoral outcomes outlined below (while noting that both political parties have expressed interest in promoting the development of generic drugs, lowering drug prices, and containing healthcare costs; and the two parties have also been focusing on antitrust, platform liability, and privacy issues relating to many of America’s biggest technology enterprises):

- If President Trump is re-elected and wins the White House, Democrats keep control of the House of Representatives, and Republicans keep control of the Senate, such an outcome would likely favor securities in the following sectors: technology, defense, finance, healthcare, and energy, while potentially putting pressure on sectors and companies that could be harmed by further deterioration in U.S-China relations;

- If Vice President Biden wins the White House, Democrats keep control of the House of Representatives, and Republicans keep control of the Senate, such an outcome would likely favor companies and sectors that would be deemed to have thereby avoided increased taxes and a heavier regulatory burden;

- If Vice President Biden wins the White House, Democrats keep control of the House of Representatives, and Democrats take control of the Senate(sometimes referred to in the media as a “blue wave”), such results would substantially raise the odds of higher taxes. Offsets to the latter outcome could come in the form of substantial additional spending on infrastructure, education, and healthcare. Securities in the following sectors, among others, are perceived to be disadvantaged by a “blue wave” Democratic sweep: defense, healthcare, financials (via increased regulation) and energy (with expectations of restricting fracking and limiting drilling on federal lands in Texas/New Mexico’s Delaware Basin and Southeast Montana/Northeast Wyoming’s Powder River Basin), while giving a lift to sectors and companies that could be helped by improving U.S-China relations.

The Pre- and Post-Election Tax and Spending Outlook

As shown in the panel below, the current taxation and spending policy positions of Vice President Biden contain numerous base-broadening elements that increase taxes by approximately $4 trillion, while increasing spending to the tune of approximately $6 trillion in areas including healthcare, infrastructure, education, energy research, and other initiatives.

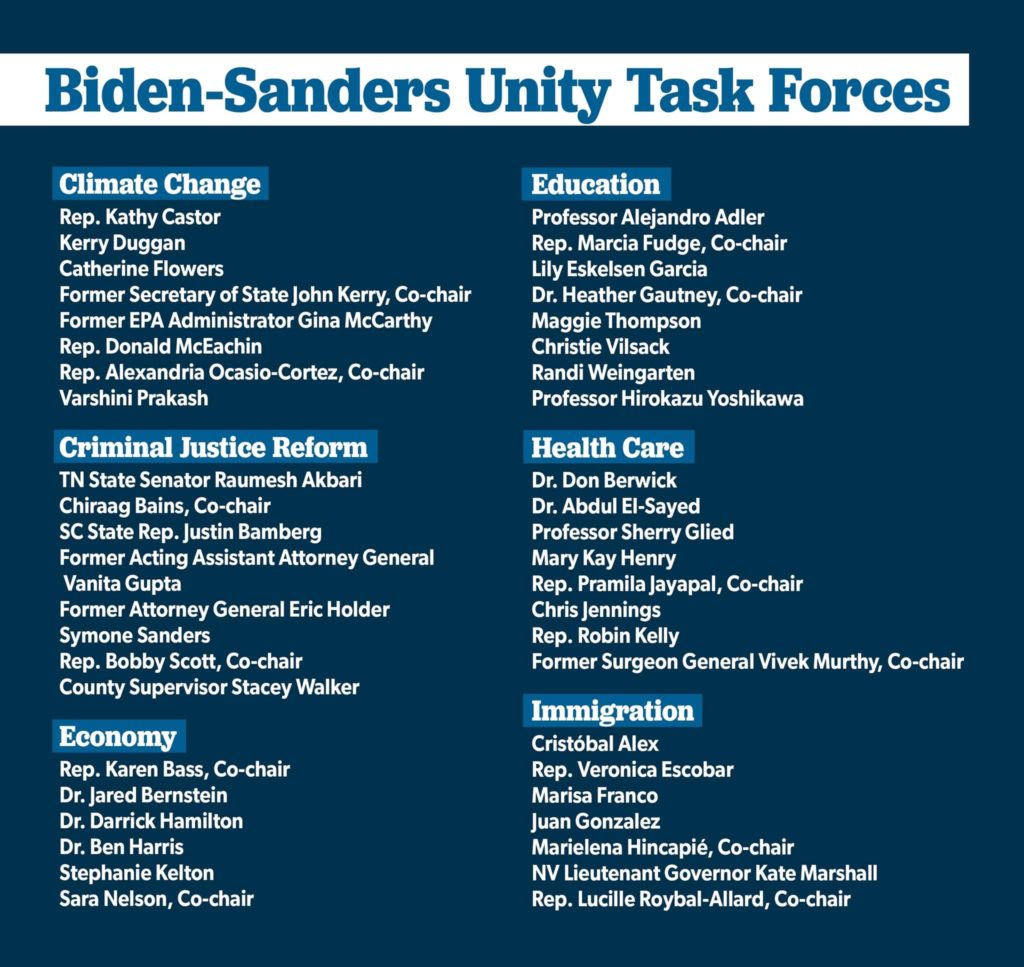

Released on Wednesday, July 9, the 110-page report of the Unity Task Forces (created and staffed by individuals designated by Vice President Joe Biden and Senator Bernie Sanders) contains a detailed set of policy recommendations in six domestic policy areas:

- Health care (while not supporting Medicare for All, the report proposes a public option, a government-administered plan “like Medicare” that would be available to all Americans; on drug pricing, the report recommends appointing a government board to set prices that Medicare would pay for new drugs);

- The economy (with $400 billion pledged for procurement of domestically made goods and $300 billion to support high-tech research);

- Climate change (here, a total of $2.0 trillion over four years is earmarked to shift millions of jobs into clean energy, with the goal of cutting emissions from power generation to zero by 2030, having net zero emissions by 2050, and introducing new fuel-economy standards);

- Criminal justice (proposing reforms to law enforcement and policing practices);

- Education (including universal preschool for three- and four-year-olds, at a cost of $775 billion over a decade), and

- Immigration (proposing to end travel restrictions against 13 countries, and to maintain protections from deportation for approximately 700,000 young immigrants known as “Dreamers”).

Should Vice President Biden win the White House, financial asset prices in general, as well as specific industries and companies, are likely to be affected by the speed and degree to which the new Administration and Congress (whose degree of support depends on which party controls the House of Representatives and which party controls the Senate) might be able to implement priorities in these and other areas.

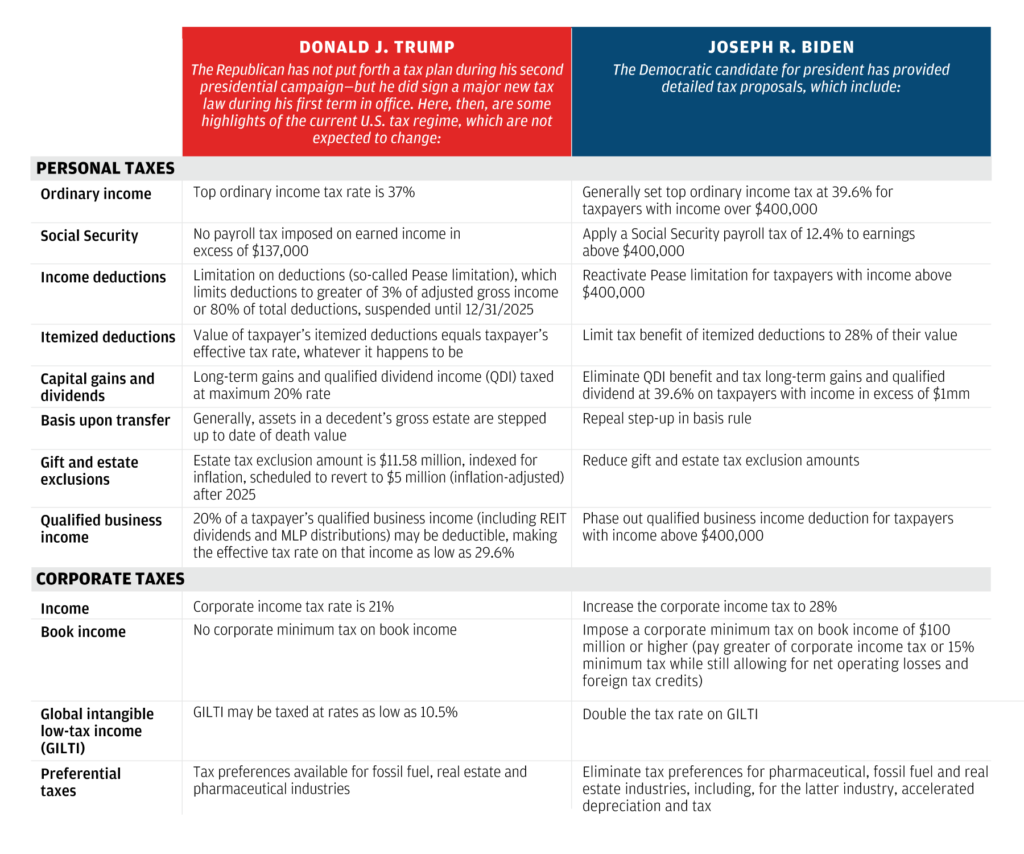

For further granularity, the following panel sets forth eight elements of personal taxes and four elements of corporate taxes: (i) under the current U.S. tax regime, which would not currently be expected to change much under President Trump (although the President has endorsed the idea of payroll tax reductions; tweeted about a potential capital gains cut; and vowed to extend the Tax Cuts and Jobs Act of 2017, which capped the so-called SALT (State and Local Tax) deduction at $10,000); and (ii) as currently outlined as taxation policy under a Biden administration.

Given that the process of turning taxation proposals into law takes time, it is likely to be at least June 2021 for new tax legislation to be enacted. On several aspects of tax planning (including the timing and forms of income and expenditures; tax gain-loss harvesting; and retirement, estate, and gifting strategies), it may be sensible to postpone any major moves until a judicious assessment can be made of the makeup of the post-election government and its specifically-expressed legislative agenda.

Regardless of the fireworks, and ultimate outcome, of the election, we will always believe that good, well-run, profitable companies will remain good, well-run, profitable companies, independent of a Trump or Biden win.

What’s Happening at TPW?

Happy to have him aboard, contributing, and part of the Towerpoint Wealth family, the TPW team has been indoctrinating Matt Regan a.k.a. “the new guy,” over the past two weeks:

Our new Wealth Advisor, Matt Regan, connected with our President, Joseph Eschleman, and our Partner, Wealth Advisor, Jonathan LaTurner, for an enjoyable business lunch at the historic Sutter Club in downtown Sacramento earlier this week.

Our President, Joseph Eschleman, and his wife, Megan Eschleman, hosted Matt and his lovely wife Alyssa for an enjoyable evening of tri-tip, corn on the cob, chicken skewers, and Frank Familycabernet.

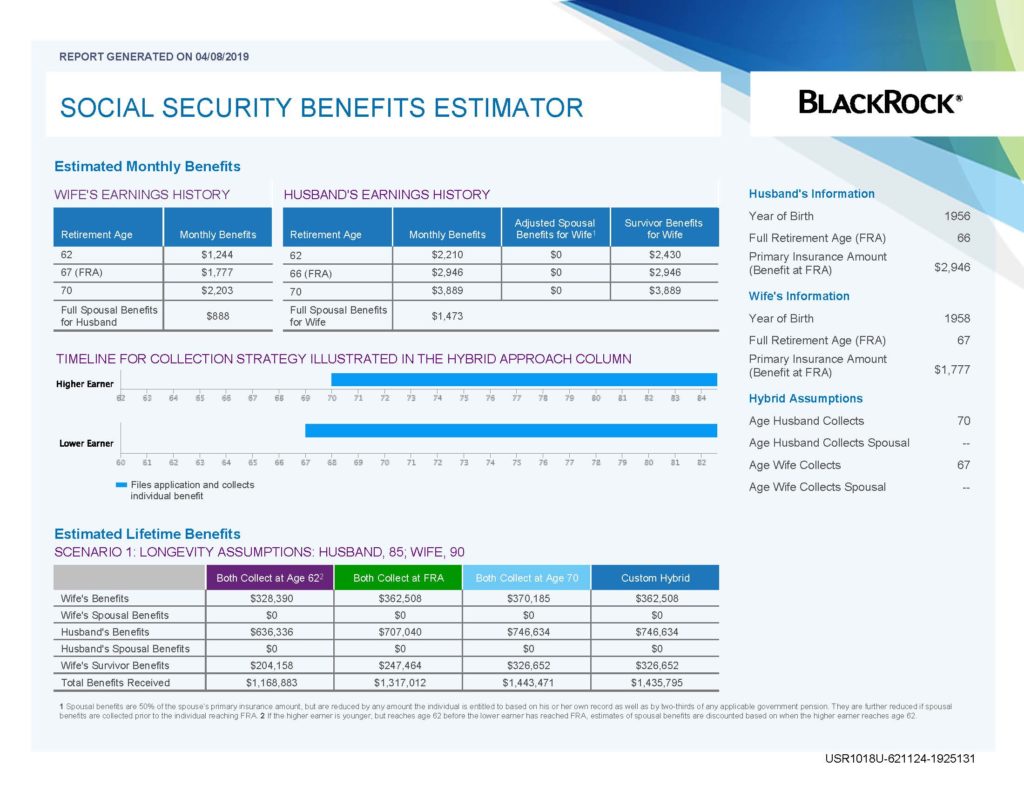

TPW Service Highlight – Social Security Optimization

Many investors are not prepared for retirement, and have not properly planned for how to structure their post-retirement income. With the popularity and availability of pension plans quickly waning, and rock bottom interest rates making it difficult to derive enough interest income from bonds, the importance of Social Security has never been greater.

Through careful planning and the development and utilization of a custom Social Security optimization analysis, our aim at Towerpoint Wealth is to help our clients structure a plan to ensure that they are not leaving any money on table when it comes to their Social Security benefits. According to the Annual Statistical Supplement to the Social Security Bulletin, 70% (!) of all retired workers started taking benefits before their normal retirement age. For some this may make sense, but for many, this will result in the forfeiture of tens, if not hundreds of thousands of dollars over their lifetime.

Let us help you scientifically analyze the myriad of Social Security claiming strategies available to you, and develop a customized plan to ensure you have properly maximized this hugely important retirement income benefit.

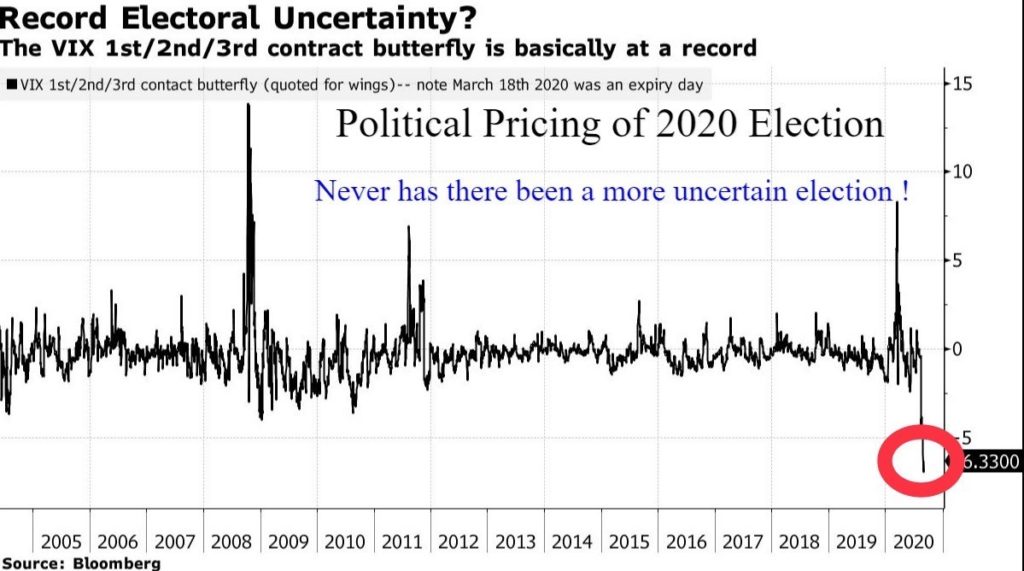

Graph of the Week

The market anticipates some pretty incredible fireworks (as we probably all do) leading up to November’s elections. With Joe Biden’s lead over President Trump drifting lower since the late summer, there is now even more expected volatility around Election Day, and things almost assuredly will only heat up further as we get closer to November.

The graph below reflects the historical activity and pricing of the VIX, a popular index that measures future stock market volatility, used by investors to hedge against it. Currently, November’s election is the most expensive event risk on record. With many more absentee and mail-in ballots expected to be cast in this election, the possibility certainly exists that we do not know who the winner is on Wednesday, November 4.

Quoting Cameron Crise, Bloomberg macro strategist, “In the history of VIX futures contracts, we’ve never had an event risk command this sort of premium… That obviously suggests that markets anticipate some pretty incredible fireworks.”

Don’t say you haven’t been warned, keep your seatbelt firmly buckled, and most importantly, don’t be surprised nor overreact to the upcoming craziness!

As always, we sincerely value our relationships and partnerships with each of you, as well as your trust and confidence in us here at Towerpoint Wealth. We encourage you to reach out to us at any time (916-405-9140, info@towerpointwealth.com) with any questions, concerns, or needs you may have. The world continues to be an extremely complicated place, and we are here to help you properly plan for and make sense of it.

- Nathan, Raquel, Steve, Joseph, Lori, Jonathan, and Matt