A Talk with Dr. Ben Bernanke, Former Chairman of the Federal Reserve

Our President, Joseph Eschleman, was recently invited to sit on a conference call led by Ben Bernanke, former Chairman of the Federal Reserve and PIMCO senior advisor. Bernanke discussed why recent policy moves made by the Federal Reserve (“the Fed”) and other central banks will be critical to a more stable future for the global economy and financial markets. Bernanke discussed why given today’s unpredictable environment, policy response must first focus on public health to promote recovery, and should be senior to current economic policy. To be clear, the role of monetary and fiscal policy, while hugely important during this pandemic, is primarily meant to keep things alive and to support the economy during this temporary economic downturn. The Fed has acted with alacrity in this current crisis to help support liquidity in the capital markets, help financial institutions have access to cash, and to keep credit flowing to the real economy. Domestically and globally, recovery will depend on 1.) public health, 2.) science and 3.) the public’s confidence in both. It will likely be slow, and with false starts, and it will assuredly be different across regions, industries, and businesses. And while 2020 will assuredly be a year of severe recession, our hope is that the economy will open up by the latter part of the year, especially as the medical situation improves, with growth prospects for 2021 being significantly better

Current Economic Environment

Bernanke did not waste any time pointing out that we are facing a deep global recession. And while there may be an emotional relationship between the COVID-19 crisis and the 2008 global financial crisis (primarily the stress created by uncertainty and similarities surrounding the extreme market volatility), the chain of causality is quite different. The ’08 recession was caused primarily by financial system dysfunction, which led to economic instability and weakness, while today’s COVID-19 recession has been caused not by problems in our financial system, but instead by a natural disaster bringing the global economy to a near standstill.

The good news is our banking system is strong and healthy, unlike in 2008. Debt issued by major banks and financial institutions has been backstopped by the Fed, and banks today are well-capitalized and a source of economic strength, opposite of the environment during the 2008 recession.

Today, the critical element will be public-health policy response to the pandemic, which is even more important than economic policy. Working towards a vaccine is obviously a critical step to recovery, with the purpose of monetary and fiscal stimulus to keep things alive in the shorter-term until a vaccine is ready and we can begin to get back to life as normal.

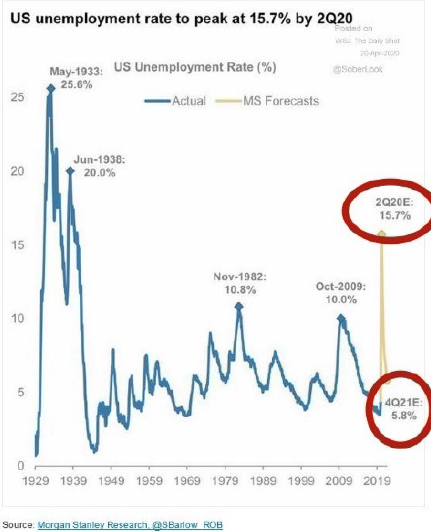

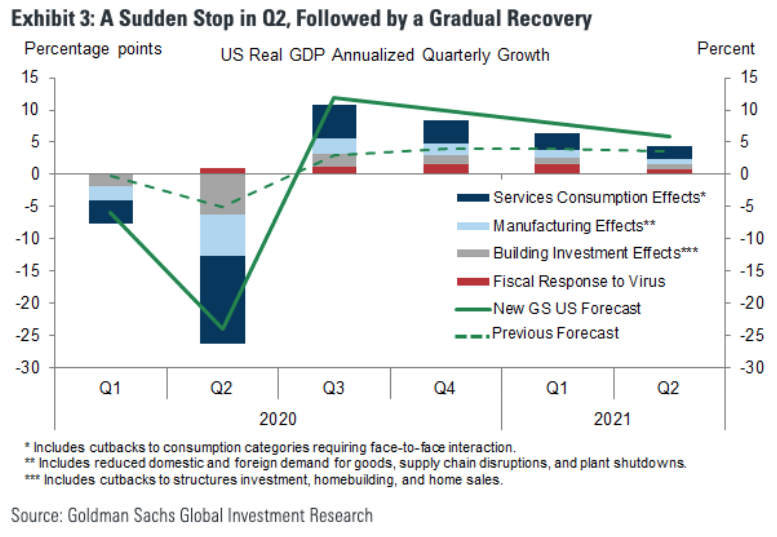

Bernanke said to expect the near-term economic numbers to be brutal, with -30% GDP and a double-digit unemployment rate here in the United States over the next few quarters. However, these unprecedented figures are expected to be temporary, and to some extent should be taken with a grain of salt. The key question: How long will the temporary shutdown last? One quarter? Two quarters? All of 2020? Longer? If it lasts through the summer, we could be looking at severe bankruptcies and permanent job losses and layoffs.

The Fed’s Toolkit

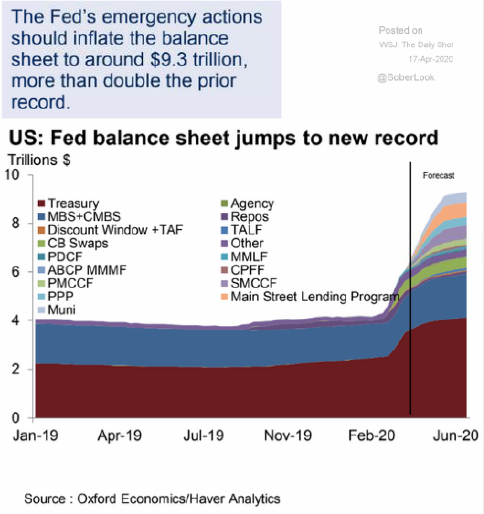

Currently, the Fed is operating at an unprecedented scale, and when compared to 2008, has already done much more, and quicker, to provide support to the economy and to the financial system. Current Fed Chair Jay Powell deserves credit for his swift decision-making, as well as his use of the monetary “playbook” that was established during the 2008 financial crisis. The Fed remains the global lender of last resort, and has already taken action to provide $2.3 trillion of loans to support the United States economy. The size of the Fed’s current balance sheet is $6 trillion (and growing), the biggest it has ever been. And while the sheer size of it concerns some economists, Bernanke was quick to point out that the Fed is acting as a lender, and not a grantor, and is lending on a collateralized basis. These loans are self-liquidating, meaning the money the Fed is loaning is being used to buy assets (bonds), which will in turn be used to then pay back the loan when the bonds mature. Over a period of time this will automatically cause the Fed’s balance sheet to shrink to a more normal level.

Additionally, the Fed recognizes that the U.S. dollar is still king, is still viewed as the world’s currency, and that the availability of dollars is critical to maintain global liquidity and to fuel global credit. Demand for dollars is very strong right now, and to satisfy that demand and to provide dollars to foreign central banks, the Fed has also opened dollar swap lines with 14 different foreign central banks, acting as a repo facility for these banks and collecting interest while doing so.

Bernanke also focused on the emergency credit programs originally introduced to deal with the strained credit conditions of the Great Depression, and utilized more recently during the 2008 financial crisis. Section 13(3) was added to the Federal Reserve Act in 1932 to expand the Fed’s lending authority beyond banks, permitting it to extend credit to individuals, partnerships, municipalities, and corporations – a type of “Main Street” lending facility. Credit markets have recently been extremely dysfunctional, and these 13(3) lending facilities have allowed the Fed to backstop the credit markets in a secure manner and reduce overall volatility. The popular Paycheck Protection Program (PPP) is authorized under section 13(3), and a $500 billion municipal liquidity facility has also been established to offer credit to state and local governments.

Monetary Policy

In addition to its lending capacity, the Fed also has monetary policy as ammunition to combat the severe economic slowdown. Short-term interest rates have been cut to zero, and the Fed is buying Treasury and mortgage-backed bonds to provide liquidity to the economy. This extremely loose monetary policy is meant to be a temporary placeholder and create an “economic bridge” until we are out of lockdown and the economy begins to pick up speed. Bernanke expressed concerns that people may start saving more and spending less after we see a loosening of the lockdown, and any additional Fed easing will be based on the pace of the economic recovery. It is going to take a while for the economy to get back on track and up and running again, with things not approaching normal in our economy until at least later 2021 and into 2022.

Negative interest rates were discussed as a possible economic policy tool in some circumstances, but the Fed is not inclined to pursue them over the near term. Why?

1. They have a very limited scope.

2. They may disrupt the money market industry.

3. They are most useful to fight deflation (see Japan in 2016), and the COVID-19 crisis is not deflationary.

4. The Fed is on record as saying they are not willing to consider negative rates.

Fiscal Policy and the Political Environment

The 2020 recession is very different when compared to 2008’s recession. It may sound surprising, but Congress is significantly more bi-partisan about today’s economic crisis than they were in ’08. Today, we are fighting a common problem – the virus; in 2008, the problem was the health of our banks, and bailing out the banks was an extremely unpopular issue. The fiscal response to today’s crisis has been very good, and Bernanke believes we will need more from fiscal policy as the economy begins to open back up. Our fiscal response is a de-facto relief package due to a natural disaster, but absolutely necessary to avoid even greater economic pain.

The United States is fortunate in our capacity to borrow, and demand for Treasuries is very high. The big question of how government can afford all of this stimulus and issue and backstop debt like this is a hugely important one, understanding the CARES Act was funded entirely by debt issuance. Bernanke was quick to note that he has no problems with what the U.S. has done to borrow substantially to stave off this crisis, especially understanding the financial burden of doing so is minimal with interest rates close to zero. Emergencies like the coronavirus pandemic are exactly why the United States has a deep debt capacity, although we certainly do need to do better longer-term planning about the structure of the U.S. budget.

Forward Guidance, Outlook and Recovery

It is clear that the shape, and extent, of the current recession will be directly correlated to the health response to COVID-19. Recovery will be directly correlated to the level of focus, energy, and resources placed on medicine, science, and public health. A vaccine may not be available for 12 to 18 months, and opening up the economy will be a slow and regional process, with false starts a reasonable expectation. How to keep proper distance between workers, and how to regularly test the work force for COVID-19 are key questions that will impact what the recovery will look like, as well as the seasonality of the virus. Hopefully the beginnings of a recovery begin this summer, although it remains to be seen if it will be “V” or “U” shaped, or possibly a more uneven “W” shape. Public confidence is key, as this is obviously a highly uncertain environment that requires caution and care. Bernanke holds hope that 2021 should be significantly better than 2020, as some of this year’s economic figures will be Depression-esque.

However, the Great Depression lasted 12 years, and we are hopeful this recession will be measured in months. And understanding the IMF made huge changes to its global growth expectations for 2020 (from +3% to -3%), their 2021 forecast is for growth of +6%.

The United States is institutionally strong (governors, mayors, CEOs, presidents of universities, etc.), having high levels of diversity and innovation. As a country, we have weathered many other crises in our collective past, each of which was unique in its circumstances and impact, and we are confident that this pandemic will prove to be no different.

How Can We Help?

Joseph F. Eschleman, CIMA®, President, Towerpoint Wealth

At Towerpoint Wealth, we are a fiduciary to you, and embrace the legal obligation we have to act in your best interests 100% of the time. We encourage you to call (916-405-9140) or email (info@towerpointwealth.com) to open an objective dialogue.

Towerpoint Wealth, LLC is a Registered Investment Adviser. This material is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Towerpoint Wealth, LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Towerpoint Wealth, LLC unless a client service agreement is in place.