Understanding The National Debt, the US Debt-to-GDP, and Why It Matters for Investors

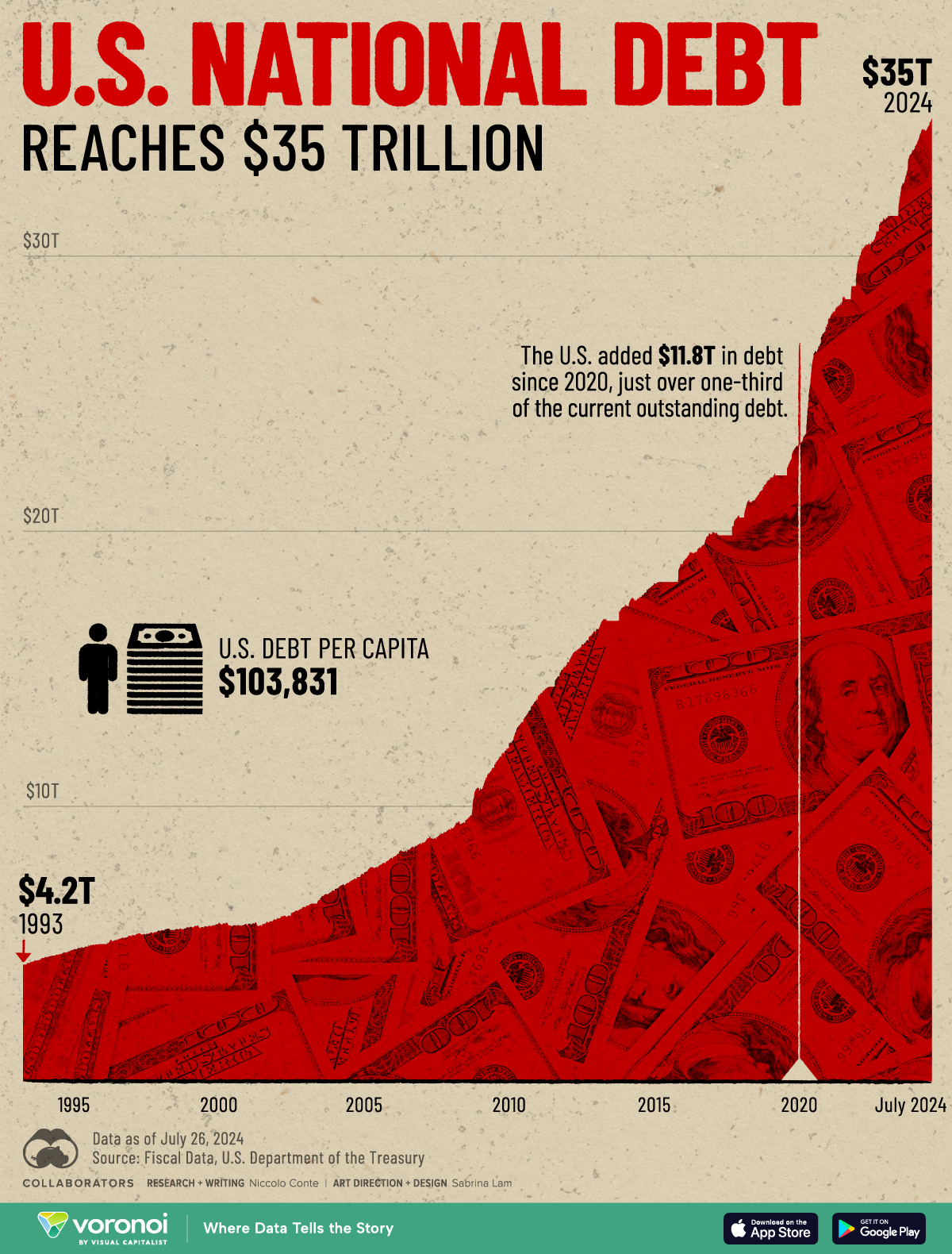

The U.S. national debt has soared to an unprecedented $35 trillion, growing by an alarming $2 trillion every year!

The growth of the federal debt regularly dominates the headlines, raising questions about the nation’s fiscal health and the debt’s potential impact on our economic stability. For investors, this escalating debt isn’t just a number in the news — it’s a factor that can shape market conditions, interest rates, and portfolio performance.

While the sheer size of the debt is concerning, it’s important to keep a focus on its sustainability. The key lies in understanding how the cost of servicing this debt — measured as a percentage of Gross Domestic Product (GDP) — can affect government policy, economic growth, and market stability.

Historically, low interest rates have shielded policymakers from feeling the full impact of rising debt, enabling expansive spending with limited fiscal restraint, but those days seem to be over. With interest burdens now returning to levels last seen in the 1990s, the U.S. faces a critical turning point.

As the global leader and issuer of the world’s reserve currency, the United States holds significant economic advantages. However, these advantages depend on responsible debt management and maintaining confidence in the dollar’s strength. The erosion of this confidence could have profound implications for global markets, economies, and investment strategies.

In this article, we’ll break down the current state of the U.S. national debt burden, examine how it impacts the value and role of the U.S. dollar in the global economy, and provide insights into what this might mean for your portfolio. By staying up-to-date and practicing proactive planning, you can navigate these challenges and position your investments for long-term success.

Key Takeaways

- The U.S. national debt has surpassed $35 trillion in 2024, with a debt-to-GDP ratio exceeding 123%, signaling rising fiscal pressures that influence market dynamics and investment strategies.

- Higher interest rates and inflation, driven by the growing debt, can impact bond yields, the stock market, and purchasing power, requiring proactive portfolio adjustments.

- Investing in global markets and inflation-protected investments can offer opportunities to hedge against domestic economic uncertainties and capitalize on broader growth trends.

- Diversification, tax-efficient strategies, and a longer-term perspective are essential for navigating the challenges of the U.S. national debt while positioning your portfolio for resilience and success.

Understanding the Current State of the U.S. Debt Burden

The best way to understand the U.S. national debt isn’t just by looking at the massive top-line figure, but by focusing on the U.S. debt-to-GDP ratio — a measure of how the federal debt compares to the size of its economy. Currently, the U.S. debt-to-GDP ratio is 123%, indicating that the country owes more than its entire annual economic output.

For context, this ratio has grown steadily over decades, fueled by government spending, tax cuts, and historically low interest rates. The Congressional Budget Office (CBO) predicts that the federal government debt will continue to outpace the nation’s economic growth.

Breaking Down the National Debt: What Investors Need to Know

The U.S. debt is divided into two main categories:

- Debt Held by the Public: This includes Treasury securities and bonds owned by individuals, corporations, state and local governments, and foreign governments. It represents the debt that directly influences markets and interest rates. Most of the domestically held public debt is owned by the Federal Reserve.

- Intragovernmental Debt: Debt held by government trust funds, like Social Security and Medicare, which reflects the government’s internal financial obligations.

For you, as an investor, public debt is especially important because it impacts everything from interest rates to inflation to fiscal policy — all of which shape broader market conditions, and can affect your portfolio’s performance.

The Rising Cost of Borrowing

For years, low interest rates helped keep borrowing costs manageable, even as the debt grew; however, that is no longer the case. In fiscal year 2023, net interest payments on the national debt rose to 2.4% of GDP, and projections suggest future interest payments could reach 3.0% in 2024 — the highest levels since the late 1990s. This spike in the debt limit, or debt ceiling, limits the government’s ability to invest in other priorities, potentially creating ripple effects across the economy.

For investors, rising interest rates can mean higher yields on bonds, but they also signal potential challenges for equity markets and economic growth. Understanding interest rates and how they affect the stock market is crucial for investors to optimize their portfolios to efficiently navigate the market — and it is equally important for policymakers to understand the role of interest rates in their policy decisions.

Why the Federal Debt Matters

The U.S. national debt isn’t just a government issue, it’s an economic reality that can affect everything from the value of the U.S. dollar to the performance of investments. As debt levels climb, so does the cost of servicing it, which poses challenges for fiscal policy and financial markets alike.

The Debt-to-GDP Ratio: A Benchmark of Fiscal Health

Think of the debt-to-GDP ratio as a metric similar to the nation’s “credit score.” A high ratio signals that debt is growing faster than the economy, which can erode confidence in the government’s ability to manage its obligations. While the U.S. is not at the level of an economic fallout (like that of Argentina), this rising ratio seems to underpin our need for sustainable fiscal policies.

For investors, a high debt-to-GDP ratio can have real-world implications:

- Rising Interest Rates: As debt levels grow, so does the cost of servicing that debt. This puts upward pressure on interest rates, which affects everything from bond yields to borrowing costs for businesses and consumers.

- Reduced Fiscal Flexibility: Higher interest payments consume a larger portion of the federal budget, limiting the government’s ability to invest in growth-driving initiatives like infrastructure, research, and education.

The U.S. Dollar and Global Confidence

The U.S. dollar’s status as the world’s reserve currency is a cornerstone of its economic power. Since World War II, this privileged position has allowed the U.S. to borrow at lower costs and maintain a dominant role in global trade and finance. However, the rising national debt poses risks to this standing.

As debt levels grow and the debt-to-GDP ratio climbs, global confidence in the dollar could weaken. If investors or foreign governments begin to question the U.S.’s ability to manage its fiscal responsibilities, demand for the dollar could decline, potentially leading to currency depreciation, reducing purchasing power and making imported goods more expensive, and higher borrowing costs, further increasing the cost of debt.

Impacts on Economic Growth

Growing national debt, as seen through historical trends in U.S. debt by the year, also has broader implications for economic growth. When the government borrows heavily, it competes with businesses and individuals for available capital. This can drive up interest rates and reduce private-sector investment, which is critical for innovation and job creation.

Persistent deficits and high debt levels can also contribute to inflation, eroding the real value of investments and reducing the purchasing power of households like yours.

Why This Matters to Investors

The federal debt directly influences market dynamics and portfolio performance. Rising interest rates, inflation, and economic uncertainty all affect asset values and investment returns. Understanding these factors can help you make informed decisions about how to allocate and diversify your investments, manage risk, and position your portfolio for resilience.

By staying proactive and working with a trusted financial advisor, you can navigate the challenges posed by the national debt and identify opportunities that align with your financial goals. At Towerpoint Wealth, we examine a myriad of market factors to help our clients navigate volatility and make informed decisions that align their investment strategies with their unique risk tolerance and financial goals.

Implications of National Debt for Investors

The growing national debt has far-reaching consequences that extend beyond the federal budget and the U.S. dollar. As discussed, when it comes to investors, the national debt directly impacts market dynamics, investment returns, and portfolio strategies. Understanding these implications can help you navigate the challenges and opportunities presented by today’s fiscal environment.

Rising Interest Rates and Bond Yields

As the government’s borrowing needs grow, it often raises interest rates to attract buyers for its debt. Higher interest rates can have a dual impact on your portfolio:

- Bond Markets: Rising rates typically lead to lower bond prices, which can negatively affect existing fixed-income investments. However, new bonds offer higher yields, creating investment opportunities for income-focused investors.

- Equity Markets: Higher interest rates increase borrowing costs for businesses, potentially slowing growth and reducing profitability, which may weigh on stock valuations.

Inflation and Purchasing Power

A growing debt burden, coupled with high inflation, erodes purchasing power. This can impact your portfolio by reducing the real value of investment gains, particularly for fixed-income assets. It can also affect inflation-sensitive sectors. While energy and commodities may see higher demand, others, such as consumer goods, may struggle with rising input costs.

Market Volatility

The growing national debt and its economic implications often contribute to heightened market volatility. As government borrowing increases and fiscal policies evolve, investors may experience more frequent and pronounced market swings. While this uncertainty can be unsettling, it also creates opportunities for those who are prepared.

To manage market volatility, it’s important to remember two key cornerstones of sound financial planning:

- Diversification: Spreading investments across asset classes and geographies to reduce risk.

- Long-Term Perspective: Staying focused on financial goals despite short-term fluctuations.

Opportunities in Global Markets

A rising U.S. national debt and the potential weakening of the dollar can create opportunities for investors to diversify internationally. When the dollar depreciates, foreign investments often gain value when converted back into U.S. dollars, enhancing overall returns. Additionally, global markets, particularly in emerging economies, may offer higher growth potential compared to the more mature U.S. market.

Key Strategies for Global Investing

- International Equities: Ask your financial advisor about established companies in developed markets or high-growth industries in emerging economies.

- Foreign Bonds: Consider diversifying fixed-income holdings with bonds from stable or growing foreign markets.

- Global ETFs and Mutual Funds: Look into simplified international investing with funds that offer broad exposure to global opportunities.

Proactive Strategies for Navigating the National Debt

As we have discussed, the growing U.S. national debt presents a complex challenge for the economy and financial markets. With the right strategies, however, investors can mitigate potential risks while capitalizing on new opportunities. Proactive planning, diversification, and informed decision-making are essential for navigating this evolving landscape.

Here’s what that may look like for investors like you:

Diversify Across Asset Classes and Geographies

Diversification remains one of the most effective ways to reduce portfolio risk, particularly in an environment of economic uncertainty driven by rising debt.

By allocating investments across various asset classes — such as equities, bonds, real estate, and alternatives — you can minimize the impact of market volatility on your overall portfolio. Diversifying globally can also provide exposure to international markets, which may benefit from a weaker U.S. dollar and offer higher growth potential in emerging economies.

Prepare for Inflation

High national debt levels often contribute to inflationary pressures, which can erode purchasing power and reduce real returns on investments. To protect your portfolio from inflation:

- Consider Investing in Inflation-Protected Securities: Treasury Inflation-Protected Securities (TIPS) and commodities, such as gold, can provide a hedge against rising prices.

- Consider Real Assets: Investments in real estate, commodities, and infrastructure often perform well in inflationary environments, offering both present income and potential appreciation in the future.

Optimize Fixed-Income Investments

Rising interest rates — a common consequence of increasing debt — can negatively affect existing bond prices; however, it can also create opportunities for new fixed-income investments. Investing in shorter-duration bonds, for example, can provide stability, as these are less sensitive to rate changes. Newly issued higher-yield bonds are another way to increase your income while balancing risk

Leverage Tax-Efficient Strategies

As the government addresses its debt, tax policy changes may follow, making tax efficiency a critical component of your financial plan. Some strategies to consider are:

- Maximize Tax-Advantaged Accounts: Contributions to IRAs, 401(k)s, and Health Savings Accounts (HSAs) defer or eliminate taxes on investment growth.

- Implement Tax-Loss Harvesting: Offset capital gains by strategically selling underperforming assets, reducing your taxable income.

Stay Focused on Your Longer-Term Goals

Short-term volatility caused by debt-related market fluctuations can be unsettling, but maintaining a disciplined, long-term perspective is the key to long-term wealth. Performing regular portfolio reviews with your financial advisor can help make sure you periodically reassess your asset allocation and risk tolerance to stay in alignment with your plan and with your goals.

Final Thoughts

The rising U.S. national debt is a complex issue, with historical data on U.S. debt by the year providing critical insights into its accelerating growth.

This increasing debt has significant implications for the economy, markets, and your investments. While challenges like inflation, rising interest rates, and market volatility may feel daunting, they also present opportunities for proactive and informed investors.

By diversifying globally, protecting against inflation, leveraging tax-efficient strategies, and staying focused on long-term goals, you can position your portfolio for resilience and growth in an uncertain economic landscape.

At Towerpoint Wealth, we’re here to help you navigate these complexities with personalized strategies tailored to your risk tolerance and financial objectives. If you’re ready to take control of your financial future in the face of today’s challenges, we invite you to schedule a consultation with our team. Together, we can build a plan that helps you thrive, regardless of what the future holds.